📋 Quick Summary:

- Despite billions invested, Michigan still faces a significant shortage of affordable housing units.

- Assistance programs vary by income, household size, and location, requiring proactive and tailored efforts.

- Navigating programs and eligibility depends on local contacts, documentation, and continuous follow-up.

Michigan has invested billions in affordable housing, yet many residents still struggle to find real help. In fiscal year 2025, MSHDA supported 45,000 households with $2.61 billion in funding and produced over 12,000 new housing units statewide. Despite that scale, the need still outpaces the supply. If you are a renter, a first-time buyer, or a family stretched thin by housing costs, the right program can genuinely change your situation. This guide walks you through Michigan’s key affordable housing programs, who qualifies, how to apply, and what to expect at every step.

Table of Contents

- Understanding affordable housing in Michigan

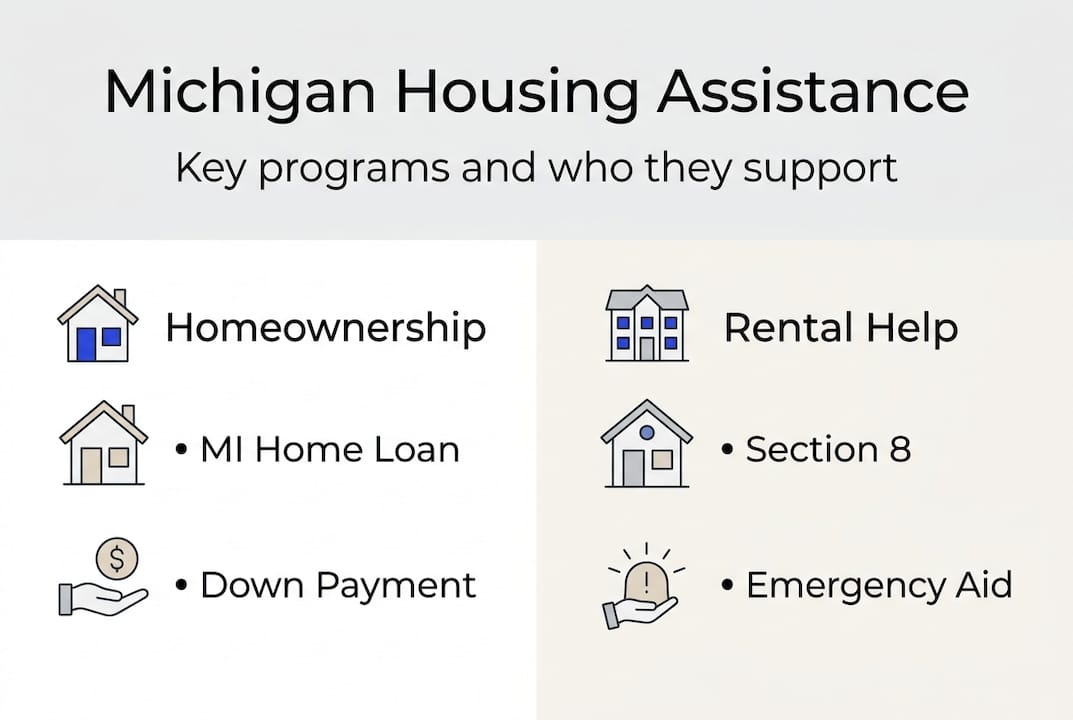

- Statewide affordable housing programs: MSHDA explained

- MSHDA homeownership options: MI Home Loan and Down Payment Assistance

- Rental assistance and Housing Choice Vouchers (Section 8)

- Current challenges and new directions for affordable housing in Michigan

- Why one-size-fits-all solutions fall short: What Michigan residents really need

- Take the next step with guidance and local expertise

- Frequently asked questions

Key Takeaways

Understanding affordable housing in Michigan

Affordable housing is not just a political term. It has a specific, practical meaning: housing that costs no more than 30% of a household’s gross monthly income. When rent or a mortgage payment pushes past that threshold, a family is considered “cost-burdened,” meaning they have less money left for food, healthcare, and other basics. Michigan faces a real and growing challenge on this front. 36% of Michigan renters are cost-burdened, paying more than they can reasonably afford each month. Families in cities like Detroit, Flint, and Lansing feel this pressure acutely, but suburban areas are not immune. Residents exploring affordability challenges in Oakland County will find that even higher-income communities have pockets of serious housing stress. So who qualifies for help? Eligibility varies by program, but most assistance is based on:

- Household income relative to the Area Median Income (AMI)

- Household size (larger families may qualify at higher income thresholds)

- First-time buyer status or residency in a targeted area

- Rental status and local waitlist availability

- Special circumstances such as disability, veteran status, or homelessness risk

“Affordable housing is not a handout. It is a structured system designed to stabilize families and create pathways to long-term economic security.”

The Michigan State Housing Development Authority (MSHDA) is the primary state body coordinating these efforts. Understanding what MSHDA offers is the first real step toward accessing help. If you have felt stuck or overwhelmed before, these tips for frustrated home buyers can help you reset and move forward. Pro Tip: Eligibility rules and waitlists change frequently. Check MSHDA’s website and your local housing agency at least once a quarter to stay current.

Statewide affordable housing programs: MSHDA explained

With a framework for understanding affordable housing, it is time to meet the organization at the center of Michigan’s solutions: MSHDA. MSHDA is the primary state agency administering affordable housing programs in Michigan, including homeownership loans, down payment assistance, rental vouchers, and developer funding. In fiscal year 2025, MSHDA invested $2.61 billion supporting 45,000 households across the state.  Here is a quick look at MSHDA’s core programs:

Here is a quick look at MSHDA’s core programs:

MSHDA also partners with local governments and nonprofits to fund new construction and rehabilitation of existing units. These program innovation results show how creative approaches are expanding supply in underserved communities. For buyers who want to think beyond traditional financing, exploring creative financing methods in Oakland County can open doors that a standard mortgage search might miss. Pro Tip: You cannot apply directly to MSHDA for homebuyer programs. All applications must go through an MSHDA-approved lender, so start by finding one in your area.

MSHDA homeownership options: MI Home Loan and Down Payment Assistance

Now that you know what MSHDA offers, let’s focus on homeownership and how to leverage these programs for your purchase.  The MI Home Loan is a 30-year fixed-rate mortgage available in FHA, VA, USDA, and conventional formats. It is designed for first-time buyers, though repeat buyers in designated targeted areas also qualify. Key requirements include a minimum credit score of 640, a down payment of 1 to 3%, and compliance with income limits by county, which range from roughly $114,720 for a one to two person household in Alcona County up to $182,000 in higher-cost areas.

The MI Home Loan is a 30-year fixed-rate mortgage available in FHA, VA, USDA, and conventional formats. It is designed for first-time buyers, though repeat buyers in designated targeted areas also qualify. Key requirements include a minimum credit score of 640, a down payment of 1 to 3%, and compliance with income limits by county, which range from roughly $114,720 for a one to two person household in Alcona County up to $182,000 in higher-cost areas.

The MSHDA down payment assistance program now offers up to $25,000 for qualifying first-generation buyers. This means buyers whose parents never owned a home. Parental wealth transfers disqualify you from this specific tier, so be prepared to document your family’s homeownership history. Here is how the application process works:

- Complete a MSHDA-approved homebuyer education course

- Check your income and credit against county-specific limits

- Find an MSHDA-approved lender in your area

- Submit your application and supporting documents through that lender

- Receive your loan commitment and pair it with DPA if eligible

Learning about down payment assistance programs and reviewing your first-time homebuyer down payment options can help you understand exactly what to bring to that first lender conversation. If you are considering an FHA loan, brushing up on FHA loan basics will give you a strong foundation before you apply. Pro Tip: First-generation DPA is generous, but it comes with strict documentation. Gather proof of your parents’ rental or non-ownership history before you sit down with a lender.

Rental assistance and Housing Choice Vouchers (Section 8)

Beyond mortgages and ownership, Michigan also offers robust programs for renters in need. The Housing Choice Voucher (HCV) program, commonly known as Section 8, helps low-income renters pay for housing in the private market. The voucher covers a portion of the rent directly, and the tenant pays the difference. It is one of the most impactful tools available for families who are not yet ready to buy. Applying for HCV works through your local Public Housing Agency (PHA), not MSHDA directly. You join a waitlist, attend a mandatory eligibility briefing when contacted, and go through annual recertification to maintain your voucher. Portability is also allowed, meaning you can transfer your voucher to another region if needed. Here is what you should prepare before applying:

- Proof of income for all household members

- Government-issued ID for adults in the household

- Social Security numbers for all household members

- Rental history and landlord contact information

- Documentation of any disabilities or special circumstances

- Current contact information that you can keep updated

“Missing a PHA notification because your phone number changed can set you back months or even years on a waitlist. Staying reachable is not optional.”

Some edge cases are worth knowing. Students under 24 who are claimed as dependents may lose HCV eligibility. Families cannot use vouchers for units owned by a family member unless a disability is involved. If a household becomes overcrowded, a new voucher may be required rather than simply adding members to an existing one. For a full list of rental assistance programs available in Michigan, MSHDA’s rental page is the most current and complete resource. Pro Tip: Update your contact information with your local PHA every time anything changes. Missing one letter or call can cost you your spot on the waitlist.

Current challenges and new directions for affordable housing in Michigan

Even with significant state investment, big challenges remain. Let’s look at what is still missing and where Michigan is innovating. Despite MSHDA’s record investments in FY25, including 5,245 new homeowners and $775 million in mortgages and DPA, a shortage of roughly 119,000 affordable units persists statewide. That gap does not close overnight. The Shelter Diversion pilot program is one bright spot, having housed more than 1,400 individuals who were at risk of homelessness.

- Modular and manufactured home construction to reduce build costs

- Local zoning reforms to allow more density in suburban communities

- Expanded DPA for moderate-income buyers who fall just above current limits

- Employer-assisted housing programs tied to workforce development

The Farmington Hills housing shortage reflects a pattern seen across Oakland County, where demand for affordable inventory consistently outpaces what is available. Keeping up with program innovations at the state level can help you spot new opportunities as they open.

Why one-size-fits-all solutions fall short: What Michigan residents really need

Here is something that most housing guides will not tell you: the biggest barrier to accessing affordable housing in Michigan is not income. It is information overload combined with a lack of personalized guidance. Every county has different income limits. Every program has different documentation requirements. A buyer who qualifies in Alcona County may not qualify in Oakland County under the same program. A renter with a disability has different HCV rights than a student living alone. These distinctions matter enormously, and a generic checklist will not capture them. The residents who succeed are the ones who treat this process like a job. They gather documents early, call their local PHA or MSHDA-approved lender before they think they are ready, and follow up consistently rather than waiting to be contacted. If you are feeling uncertain about where to start, these homebuyer tips for 2025 offer a grounded starting point. The programs exist. The funding is real. What bridges the gap is an informed, proactive approach tailored to your specific situation, not a one-size solution applied to everyone.

Take the next step with guidance and local expertise

Understanding Michigan’s affordable housing programs is a strong first step, but navigating the details on your own can still feel overwhelming.  Tom Gilliam at RE/MAX Classic has spent over 20 years helping buyers across Oakland County, including Farmington Hills, Novi, Northville, and West Bloomfield, find homes that fit their budget and their lives. Whether you are exploring DPA options, evaluating loan types, or simply trying to understand what you can afford, Homes2MoveYou.com offers resources built for real buyers in real markets. Start with the home buying guide or walk through the full home buying process to see exactly what comes next.

Tom Gilliam at RE/MAX Classic has spent over 20 years helping buyers across Oakland County, including Farmington Hills, Novi, Northville, and West Bloomfield, find homes that fit their budget and their lives. Whether you are exploring DPA options, evaluating loan types, or simply trying to understand what you can afford, Homes2MoveYou.com offers resources built for real buyers in real markets. Start with the home buying guide or walk through the full home buying process to see exactly what comes next.

Frequently asked questions

Who qualifies for affordable housing programs in Michigan?

Eligibility depends on income, household size, property location, and program rules; income limits and property caps vary by county, and many programs serve both renters and first-time buyers who meet the criteria.

How do I apply for a Michigan Housing Choice Voucher (Section 8)?

Apply through your local Public Housing Agency, join the waitlist, and attend mandatory briefings when contacted; the full process is managed through local PHAs and waitlists rather than MSHDA directly.

Can college students get affordable housing help?

Students under 24 who are claimed as dependents may be ineligible for Housing Choice Vouchers, but other assistance programs may still apply depending on individual circumstances.

What is the maximum income allowed for down payment assistance in Michigan?

Limits vary by county and household size, with income examples ranging from around $114,720 for smaller households in some counties to over $182,000 in higher-cost areas.

Is affordable housing in Michigan improving?

Progress is real, with billions invested and new pilots launched, but a 119,000 unit shortage means the statewide gap between supply and demand has not yet closed.

Recommended

- Oakland County MI First-time Home Buyers: FHA Loans 101 - Homes2MoveYou.com

- Michigan Tenancy Types 2026: 30% More Realty Clarity - Homes2MoveYou.com

- Reducing Utility Costs: Smart Moves for Michigan Homes - Homes2MoveYou.com

- Creative Financing Methods: Expanding Homebuying Options - Homes2MoveYou.com

- Down Payment Assistance Programs Can Help Pave the Way to Homeownership

Check out this article next