Summary:

- Home appraisals determine property value and impact loan approvals and closing timelines.

- Proper preparation by sellers and buyers is essential for achieving a favorable appraisal outcome.

- When appraisals are low, options include requesting a reconsideration, renegotiating, or ordering a second appraisal.

A single appraisal can determine whether your Oakland County home sale closes smoothly or falls apart at the finish line. Yet most buyers and sellers treat it as routine paperwork rather than the high-stakes evaluation it truly is. The home appraisal process directly shapes your purchase price, your loan amount, and your closing timeline. Whether you're buying in Farmington Hills, selling in West Bloomfield, or relocating anywhere across Oakland County, understanding every step of this process gives you a real advantage. This guide walks you through what appraisers look for, how value is determined, and what you can do to protect your interests before, during, and after the appraisal.

Table of Contents

- What is a home appraisal and why does it matter?

- Step-by-step: The Oakland County home appraisal process explained

- How appraisers determine your home's value: Approaches and local nuances

- Getting ready: How sellers and buyers can prepare for an Oakland County appraisal

- If your appraisal is low: Options, challenges, and next steps

- Appraisal vs Inspection: What Oakland County buyers and sellers need to know

- What most buyers and sellers miss about appraisals in Oakland County

- Get local expertise for your next Oakland County real estate move

- Frequently asked questions

Key Takeaways

What is a home appraisal and why does it matter?

A home appraisal is a licensed professional's independent opinion of a property's market value, based on physical inspection, comparable sales data, and established valuation methods. Lenders require appraisals for virtually every financed real estate transaction because they need assurance that the collateral backing the loan is worth what they're lending. Without this step, buyers could borrow far more than a home is actually worth. Appraisers in Michigan follow the Uniform Standards of Professional Appraisal Practice (USPAP), a nationally recognized code of ethics and methodology. Fannie Mae also requires appraisals to conform to the Uniform Appraisal Dataset (UAD), which standardizes how data is reported. These frameworks exist to keep the process objective and consistent across every transaction. Here's what makes appraisals so consequential for Oakland County buyers and sellers:- For buyers: An appraisal acts as a financial safeguard. If a home is listed above its true market value, the appraisal prevents you from overpaying.

- For sellers: In a rising market, appraisals can feel like an obstacle. If comparable sales haven't caught up to current demand, your appraised value may fall short of your asking price.

- For lenders: The appraised value sets the ceiling for your loan. A lower value means a smaller loan, regardless of the agreed purchase price.

Appraisals protect both buyers and lenders from overpaying; in fast-moving markets, they can frustrate sellers when values lag behind current demand.In Oakland County, the median sale price reached approximately $340,000 as of early 2026, with appraisal fees typically ranging from $300 to $500. That fee is a small price for the protection and clarity an appraisal provides. For more guidance on navigating this step as a buyer, review these appraisal tips for buyers specific to the Farmington Hills and Oakland County market. Now that you see the need, let's break down what actually happens during an appraisal.

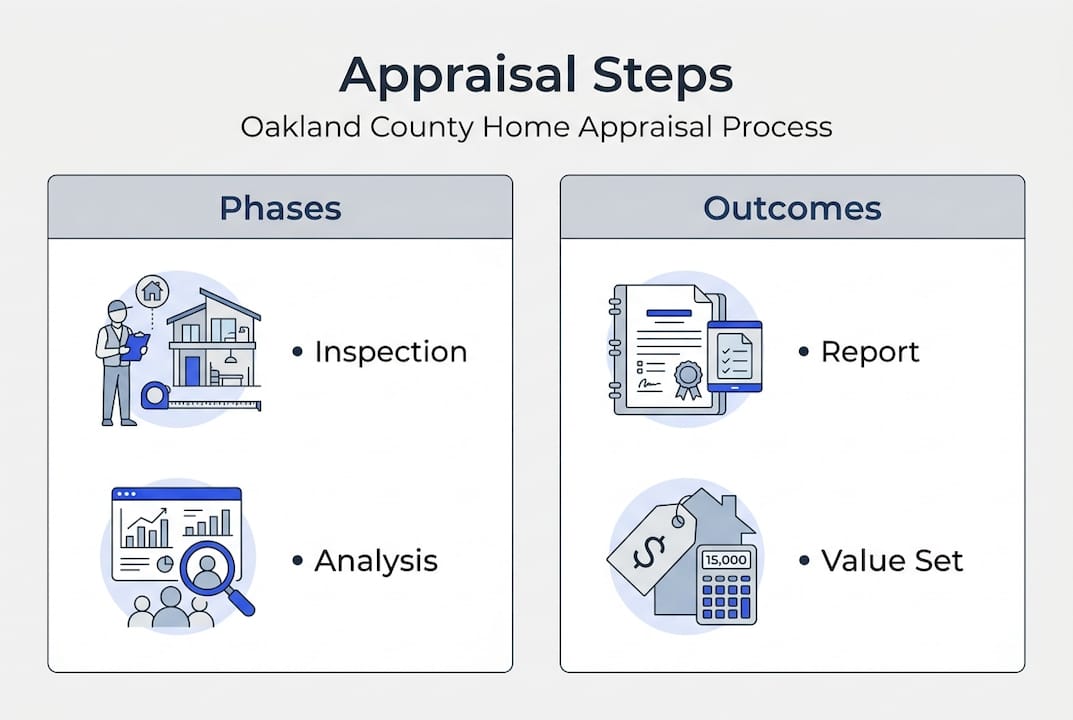

Step-by-step: The Oakland County home appraisal process explained

The appraisal process follows a structured sequence that every licensed appraiser must complete. Knowing each phase helps you stay prepared and avoid surprises.- Assignment definition. The appraiser receives the order, typically from the lender through an Appraisal Management Company (AMC). They define the scope of work, the intended use, and the property rights being appraised.

- Property inspection. The appraiser visits the home for roughly 30 to 45 minutes. They measure the square footage, photograph each room and the exterior, note the condition, and identify upgrades or deficiencies.

- Data collection. Using the MLS, public records, and county data, the appraiser gathers recent comparable sales, known as comps, typically within the past six to twelve months and within a reasonable geographic radius.

- Applying valuation approaches. The appraiser applies one or more of three recognized methods: the sales comparison approach, the cost approach, or the income approach.

- Reconciliation. The appraiser weighs the results of each approach and arrives at a final opinion of value.

- Report delivery. The completed report is delivered to the lender, usually within one to seven business days.

How appraisers determine your home's value: Approaches and local nuances

The method an appraiser uses depends on the property type and the availability of comparable data. In Oakland County, the sales comparison approach is the standard for most residential homes. This method compares your home to recently sold properties with similar characteristics: square footage, bedroom and bathroom count, lot size, age, condition, and location. The appraiser then makes dollar adjustments for differences between your home and each comparable. These adjustments can be calculated using paired sales analysis (comparing two nearly identical homes that differ in one feature), regression analysis (statistical modeling), or a cost-to-cure method (estimating the cost to fix a deficiency). The primary methodology is sales comparison, adjusted for key differences between the subject property and comparable sales.

This method compares your home to recently sold properties with similar characteristics: square footage, bedroom and bathroom count, lot size, age, condition, and location. The appraiser then makes dollar adjustments for differences between your home and each comparable. These adjustments can be calculated using paired sales analysis (comparing two nearly identical homes that differ in one feature), regression analysis (statistical modeling), or a cost-to-cure method (estimating the cost to fix a deficiency). The primary methodology is sales comparison, adjusted for key differences between the subject property and comparable sales.

- Online valuations (AVMs) like Zestimates are useful for a rough estimate, but online valuation accuracy is limited, especially for homes with unique features like lakeshore access or custom finishes.

- Tax-assessed values (SEV) in Michigan are calculated at 50% of estimated market value and are updated on a lag. They are not used in real estate appraisals and should not be your pricing benchmark.

Getting ready: How sellers and buyers can prepare for an Oakland County appraisal

Preparation is where you have the most control over the outcome. Both sellers and buyers play a role in making the appraisal go smoothly. For sellers, focus on these priorities:- Complete minor repairs before the visit. Leaky faucets, broken fixtures, and peeling paint can signal deferred maintenance and reduce value.

- Declutter and clean every room. A tidy home photographs better and allows the appraiser to assess the space accurately.

- Improve curb appeal. First impressions count, even for appraisers.

- Prepare a one-page summary of recent upgrades: roof replacement, kitchen remodel, HVAC updates, and finished basement details with approximate costs and dates.

Sellers should organize documentation, complete repairs, declutter, and improve curb appeal before the appraiser's visit to support the strongest possible valuation.For buyers, your preparation looks different:

- Review the comparable sales your agent used to justify the offer price. If those comps are strong, share them with your lender so they can be made available to the appraiser.

- Ask your agent whether the property has any unique features that could be misunderstood without context, such as a private lake lot or a high-end custom build.

- Stay in close communication with your lender about the appraisal timeline so you're not caught off guard.

- Finished basements add measurable value here, but appraisers typically value below-grade space at a lower rate than above-grade living area. Document the quality of finishes clearly.

- Lakeshore and waterfront properties require appraisers with specific local experience. Confirm your lender is using someone familiar with Oakland County's lake communities.

If your appraisal is low: Options, challenges, and next steps

A low appraisal doesn't have to kill your deal. It does require a clear-headed response and quick action. Low appraisals arise due to market lags, unique homes, condition issues, or poor comps. The main remedies are a Reconsideration of Value (ROV), renegotiation, or a second appraisal. Here are your primary options, in order of typical use:- Request a Reconsideration of Value (ROV). Your agent or lender submits a formal request to the appraiser with stronger comparable sales or factual corrections. This is not about pressuring the appraiser. It's about providing evidence they may have missed.

- Renegotiate the purchase price. Buyers can request a price reduction to match the appraised value. Sellers may agree, especially if they need to close quickly.

- Split the difference. Both parties agree to meet somewhere between the appraised value and the original purchase price. The buyer covers the gap in cash.

- Order a second appraisal. If the first appraisal contains clear errors or used inappropriate comps, a second opinion may be warranted. This typically requires a new lender or a formal dispute process.

- Walk away. Buyers with an appraisal contingency in their contract can exit the deal without penalty if the value falls short.

Custom and luxury homes in Oakland County are especially vulnerable to low appraisals because comparable sales are scarce. Document every premium feature in detail.For more strategies, review expert options for low appraisals and learn how to interpret the numbers by reading your appraisal report line by line.

Appraisal vs Inspection: What Oakland County buyers and sellers need to know

One of the most common points of confusion among Oakland County home buyers is the difference between a home appraisal and a home inspection. These are two completely separate steps in the transaction process and understanding the distinction can save you from a costly misunderstanding. A home appraisal is ordered by the lender and performed by a licensed appraiser. Its sole purpose is to determine the market value of the property so the lender knows how much they can safely loan. The appraiser is not looking for problems — they are determining value. A home inspection is ordered by the buyer and performed by a licensed home inspector. Its purpose is to identify physical defects condition issues and safety concerns throughout the property. The inspector is not determining value — they are looking for problems. Here is a simple way to remember the difference:- The appraisal protects the lender by confirming the home is worth the loan amount

- The inspection protects the buyer by revealing the physical condition of the property

- Both are required in most Oakland County financed transactions and both happen during the contingency period

- A home can appraise at full value and still have significant inspection issues — and vice versa

What most buyers and sellers miss about appraisals in Oakland County

Here's the honest truth: most sellers price their homes based on what they want to net, not what the market will actually support. They rely on online estimates or their tax assessment and then feel blindsided when the appraisal tells a different story. Tax assessments in Michigan lag the market by design. Online tools don't walk through your home. Neither one reflects what a qualified appraiser sees on the ground in your specific neighborhood. The sellers and buyers who navigate appraisals successfully share one trait: they treat the process as a dialogue, not a verdict. They gather strong evidence, communicate openly with their agent and lender, and focus on what they can control. Trying to manipulate the outcome or pressure an appraiser almost always backfires. Appraisals protect lenders and buyers but are often seen as a barrier. Your real leverage comes from preparation and understanding, not wishful thinking. If you're feeling overwhelmed by the market, these tips for frustrated buyers offer a grounded perspective on staying focused. Knowledge is your most powerful tool in any Oakland County transaction.Get local expertise for your next Oakland County real estate move

Navigating the appraisal process is far easier when you have an experienced local specialist in your corner. Tom Gilliam at RE/MAX Classic has guided buyers and sellers through hundreds of Oakland County transactions, helping them understand valuations, prepare effectively, and respond strategically when challenges arise. Explore marketing tips for sellers to position your home for the strongest possible appraisal and sale. Buyers can review the full buying process guide for step-by-step support from offer to closing. Ready to take the next step? Visit Homes2MoveYou.com to connect with Tom and access the local expertise that makes a real difference in Oakland County.

Explore marketing tips for sellers to position your home for the strongest possible appraisal and sale. Buyers can review the full buying process guide for step-by-step support from offer to closing. Ready to take the next step? Visit Homes2MoveYou.com to connect with Tom and access the local expertise that makes a real difference in Oakland County.

Frequently asked questions

How long does a home appraisal take in Oakland County?

Appraisers typically spend 30 to 45 minutes on site, with the full written report delivered to the lender within one to seven business days depending on complexity and workload.What if the appraisal comes in lower than my purchase price?

You have several options: challenge the result with an ROV, renegotiate the price with the other party, cover the gap in cash, or request a second appraisal. Low appraisal remedies depend on the contract terms and both parties' flexibility.Are online valuations like Zestimates accurate for Oakland County?

Online tools offer a rough starting point but lack local accuracy for homes with unique features, waterfront access, or custom finishes that automated models cannot assess.How does the Oakland County appraisal affect my mortgage?

The lender bases your loan maximum on appraised value; if the appraisal comes in below the purchase price, you may need to bring more cash to closing or renegotiate the deal.Is my tax-assessed value the same as my home's appraisal?

No. Michigan's tax-assessed values lag behind market conditions and are calculated differently. They are not used by buyers, sellers, or lenders to determine fair market value.What is the difference between a home appraisal and a home inspection in Michigan?

A home appraisal is ordered by the lender to determine the market value of the property. A home inspection is ordered by the buyer to identify physical defects and condition issues. Both are separate steps in the transaction. The appraisal protects the lender while the inspection protects the buyer. Both are essential in most Oakland County financed real estate transactions.Recommended

- How to Read an Appraisal Report for Oakland County Homes - Homes2MoveYou.com

- Essential Steps to Buying a Home in Oakland County, MI - Homes2MoveYou.com

- Property Taxes Explained: Complete Oakland County Guide - Homes2MoveYou.com

- Oakland County Property Taxes Guide 2025 for Homeowners - Homes2MoveYou.com

Check out this article next