Buying a home in Oakland County feels different when property prices push beyond conventional loan limits. Many first-time buyers are discovering that jumbo loans open doors to neighborhoods once thought out of reach. Understanding the real rules about jumbo loans, from stricter credit requirements to changing myths about rates, is crucial as you search for the right financing path in Michigan’s competitive market.

Pro tip: Before pursuing a jumbo loan, obtain a comprehensive financial review and speak with a local mortgage specialist who understands the unique market dynamics of Oakland County real estate markets.

Pro tip: Before selecting a jumbo loan, obtain mortgage pre-approval and carefully compare multiple lender offerings to secure the most competitive terms for your specific financial situation.

Local mortgage specialists in Oakland County understand that jumbo loans are not one-size-fits-all products. Each loan is meticulously crafted to match the borrower’s specific financial circumstances, with lenders considering factors like future income potential, investment portfolio, and long-term financial goals. This personalized approach ensures that qualified buyers can access the financing needed to purchase their dream homes in the county’s most desirable neighborhoods.

Pro tip: Work with a local mortgage professional who specializes in Oakland County real estate to develop a comprehensive financial strategy that maximizes your jumbo loan approval potential.

Local mortgage specialists in Oakland County understand that jumbo loans are not one-size-fits-all products. Each loan is meticulously crafted to match the borrower’s specific financial circumstances, with lenders considering factors like future income potential, investment portfolio, and long-term financial goals. This personalized approach ensures that qualified buyers can access the financing needed to purchase their dream homes in the county’s most desirable neighborhoods.

Pro tip: Work with a local mortgage professional who specializes in Oakland County real estate to develop a comprehensive financial strategy that maximizes your jumbo loan approval potential.

The financial landscape of jumbo loans in Oakland County reflects the region’s unique real estate dynamics. Borrowers should anticipate more complex qualification processes, with lenders requiring extensive documentation and demonstrating a robust financial foundation. This approach ensures that high-value home purchases align with both the borrower’s long-term financial goals and the lender’s risk management strategies.

Pro tip: Develop a comprehensive financial strategy with a local mortgage specialist who understands the nuanced requirements of Oakland County’s jumbo loan market.

The financial landscape of jumbo loans in Oakland County reflects the region’s unique real estate dynamics. Borrowers should anticipate more complex qualification processes, with lenders requiring extensive documentation and demonstrating a robust financial foundation. This approach ensures that high-value home purchases align with both the borrower’s long-term financial goals and the lender’s risk management strategies.

Pro tip: Develop a comprehensive financial strategy with a local mortgage specialist who understands the nuanced requirements of Oakland County’s jumbo loan market.

Discover how Tom Gilliam at Homes2MoveYou.com offers over 20 years of local real estate expertise to help you confidently navigate jumbo loan complexities and Oakland County’s competitive market. Don’t let financing challenges delay your next move. Visit Farmington Hills real estate services today to access tailored advice, personalized marketing, and negotiation skills designed specifically for buyers influenced by jumbo loan factors. Take control of your homebuying journey now with trusted guidance at every step.

Discover how Tom Gilliam at Homes2MoveYou.com offers over 20 years of local real estate expertise to help you confidently navigate jumbo loan complexities and Oakland County’s competitive market. Don’t let financing challenges delay your next move. Visit Farmington Hills real estate services today to access tailored advice, personalized marketing, and negotiation skills designed specifically for buyers influenced by jumbo loan factors. Take control of your homebuying journey now with trusted guidance at every step.

Table of Contents

- Defining Jumbo Loans And Common Myths

- Types Of Jumbo Loans For Michigan Buyers

- Jumbo Loan Limits And Requirements In 2026

- How Jumbo Loans Work In Oakland County

- Costs, Interest Rates, And Financial Implications

- Risks, Common Pitfalls, And Alternatives

Key Takeaways

| Point | Details |

|---|---|

| Understanding Jumbo Loans | Jumbo loans are designed for higher-value homes that exceed conventional loan limits and typically require stronger financial profiles. |

| Stricter Qualification | Borrowers must meet higher credit score standards, provide larger down payments, and show substantial cash reserves. |

| Market Competitiveness | Jumbo loan interest rates can be competitive and, in some cases, comparable to conventional mortgage rates. |

| Careful Financial Planning | Working with local mortgage professionals is critical to navigating jumbo loan requirements and structuring the best financing option. |

Defining Jumbo Loans and Common Myths

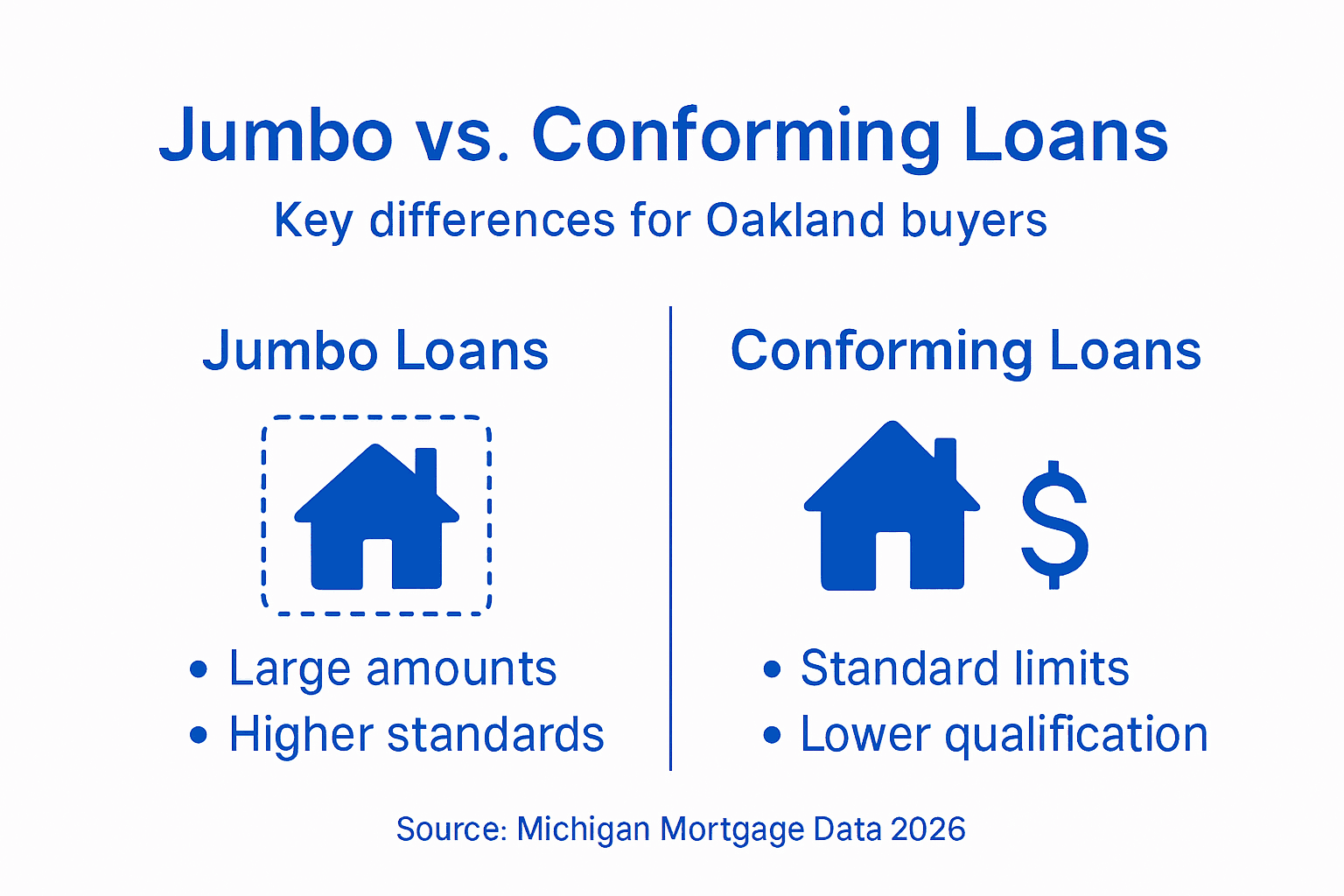

In the dynamic Oakland County real estate market, jumbo loans represent a specialized financing option for homebuyers seeking properties that exceed standard lending limits. Jumbo mortgages are unique loans designed for high-value residential properties where the loan amount surpasses the conforming loan limits established by government-sponsored enterprises Fannie Mae and Freddie Mac. Typically, jumbo loans are characterized by several distinctive features that set them apart from conventional mortgages. The loan limits can vary by region, but in most areas of the United States, they currently exceed $806,500. These loans are not backed by government entities, which means lenders assume greater risk and consequently impose more stringent qualification requirements. Potential borrowers must demonstrate exceptional financial stability through:- Higher credit scores (usually 700 or above)

- Lower debt-to-income ratios

- Substantial down payments (often 20% or more)

- Significant cash reserves

| Factor | Jumbo Loans | Conforming Loans |

|---|---|---|

| Loan Size Limit | Above $806,500 | Up to $806,500 |

| Down Payment | Typically 20% or more | As low as 3%–5% |

| Credit Score Requirement | Usually 700+ | Typically 620+ |

| Lender Risk | Higher risk with no government backing | Lower risk due to government backing |

| Qualification Process | More rigorous with extensive financial review | Standard income and asset documentation |

| Interest Rates (2026) | Approximately 6.3% | Slightly lower, but competitive |

| Who Uses It | High-value and luxury homebuyers | Most traditional homebuyers |

Types of Jumbo Loans for Michigan Buyers

In the diverse Michigan real estate market, homebuyers have access to multiple mortgage loan types that can accommodate high-value property purchases. Jumbo loans specifically offer flexible financing options for those seeking homes in premium neighborhoods across Oakland County and surrounding regions. These specialized loan products are designed to bridge the gap between conventional lending limits and the actual purchase price of more expensive residential properties. The two primary categories of jumbo loans Michigan buyers typically encounter include:- Fixed-Rate Jumbo Loans: Provide stable, predictable monthly payments with an interest rate that remains constant throughout the loan term

- Adjustable-Rate Jumbo Loans (ARMs): Feature an initial fixed-rate period followed by periodic rate adjustments based on market conditions

| Loan Type | Advantages | Drawbacks |

|---|---|---|

| Fixed-Rate Jumbo | Predictable monthly payments and long-term rate stability | Higher initial interest rates and less flexibility if rates drop |

| Adjustable-Rate Jumbo | Lower introductory rates, beneficial for short-term ownership plans | Rates can rise over time, increasing monthly payment risk |

Jumbo Loan Limits and Requirements in 2026

As the Oakland County real estate market continues to evolve, understanding the conforming loan limits becomes crucial for homebuyers seeking jumbo loan financing. For 2026, the landscape of mortgage lending presents increasingly complex requirements that potential homeowners must navigate carefully. The standard loan limit for single-family homes is projected to remain around $806,500 in most areas, with higher thresholds established for designated high-cost regions across Michigan. The key requirements for jumbo loans in 2026 are expected to include:- Credit Score Thresholds: Minimum scores of 700 or higher

- Down Payment: Typically 20% to 30% of the home’s purchase price

- Debt-to-Income Ratio: Generally limited to 43% or lower

- Cash Reserves: Sufficient funds to cover 6-12 months of mortgage payments

How Jumbo Loans Work in Oakland County

Understanding the intricacies of mortgage assistance programs is crucial for homebuyers navigating Oakland County’s competitive real estate market. Jumbo loans represent a specialized financing solution for properties that exceed standard conforming loan limits, designed specifically for high-value residential purchases in premium neighborhoods like Farmington Hills, Novi, and West Bloomfield. The mechanics of jumbo loans in Oakland County involve several distinctive characteristics:- Higher Qualification Standards: Stricter credit requirements

- Larger Down Payments: Typically 20% to 30% of home value

- Extensive Financial Documentation: More comprehensive income verification

- Personalized Underwriting: Individual loan assessment based on unique financial profile

Local mortgage specialists in Oakland County understand that jumbo loans are not one-size-fits-all products. Each loan is meticulously crafted to match the borrower’s specific financial circumstances, with lenders considering factors like future income potential, investment portfolio, and long-term financial goals. This personalized approach ensures that qualified buyers can access the financing needed to purchase their dream homes in the county’s most desirable neighborhoods.

Pro tip: Work with a local mortgage professional who specializes in Oakland County real estate to develop a comprehensive financial strategy that maximizes your jumbo loan approval potential.

Costs, Interest Rates, and Financial Implications

Navigating the complex landscape of jumbo mortgage rates requires a nuanced understanding of financial implications specific to Oakland County’s real estate market. As of early 2026, jumbo loan interest rates hover around 6.3%, reflecting a delicate balance between lending risk and market competitiveness. These rates represent more than just a number, embodying the intricate financial considerations that impact high-value home purchases in premium Michigan neighborhoods. Key financial components of jumbo loans include:- Interest Rate Structures: Fixed and adjustable-rate options

- Down Payment Requirements: Typically 20% to 30% of property value

- Closing Costs: Generally higher than conventional loans

- Additional Fees: Potential extra appraisal and underwriting expenses

The financial landscape of jumbo loans in Oakland County reflects the region’s unique real estate dynamics. Borrowers should anticipate more complex qualification processes, with lenders requiring extensive documentation and demonstrating a robust financial foundation. This approach ensures that high-value home purchases align with both the borrower’s long-term financial goals and the lender’s risk management strategies.

Pro tip: Develop a comprehensive financial strategy with a local mortgage specialist who understands the nuanced requirements of Oakland County’s jumbo loan market.

Risks, Common Pitfalls, and Alternatives

Understanding the private credit market risks is crucial for potential jumbo loan borrowers in Oakland County. High-value home financing involves complex financial dynamics that extend far beyond simple loan approval. These specialized mortgages carry significant risks that can potentially compromise a borrower’s long-term financial stability if not carefully navigated. Common risks and potential pitfalls in jumbo loan transactions include:- Market Volatility: Exposure to rapid property value fluctuations

- Default Probability: Higher risk due to larger loan amounts

- Interest Rate Uncertainty: Potential payment shock with adjustable-rate mortgages

- Limited Liquidity: Slower property resale during market downturns

Navigate Jumbo Loans Confidently with Expert Oakland County Guidance

Buying a high-value home in Oakland County requires not only understanding complex jumbo loan requirements but also partnering with a real estate expert who knows the local market inside and out. If you feel overwhelmed by higher credit standards, larger down payment demands, and detailed financial documentation jumbo loans bring, you are not alone. Securing your dream home in Farmington Hills, Novi, or West Bloomfield takes more than a loan—it takes strategy, market insight, and trusted support.

Discover how Tom Gilliam at Homes2MoveYou.com offers over 20 years of local real estate expertise to help you confidently navigate jumbo loan complexities and Oakland County’s competitive market. Don’t let financing challenges delay your next move. Visit Farmington Hills real estate services today to access tailored advice, personalized marketing, and negotiation skills designed specifically for buyers influenced by jumbo loan factors. Take control of your homebuying journey now with trusted guidance at every step.

Frequently Asked Questions

What is a jumbo loan?

A jumbo loan is a type of mortgage that exceeds the conforming loan limits set by Fannie Mae and Freddie Mac, making it suitable for financing high-value residential properties. Typically, jumbo loans have higher requirements for credit scores and down payments compared to conventional loans.What are the key requirements for qualifying for a jumbo loan?

To qualify for a jumbo loan, borrowers generally need a credit score of 700 or higher, a down payment of at least 20%, a debt-to-income ratio of 43% or lower, and sufficient cash reserves to cover 6-12 months of mortgage payments.How do jumbo loans differ from conforming loans?

Jumbo loans exceed the conforming loan limits of $806,500, require larger down payments, and typically have stricter qualification standards. In contrast, conforming loans have lower limits, allowing for lower down payments and relaxed credit requirements.What are the pros and cons of fixed-rate versus adjustable-rate jumbo loans?

Fixed-rate jumbo loans offer stable monthly payments, providing long-term predictability, but may have higher initial rates. Adjustable-rate jumbo loans feature lower starting rates but can lead to payment fluctuations, resulting in potential payment shock if rates increase.Recommended

Check out this article next