TL;DR — Key Takeaways

About 8.6% of appraisals come in below contract price nationally — and in Oakland County's luxury and lakefront markets, the risk is often higher due to thin comp pools and neighborhood-by-neighborhood price swings.

The three root causes are almost always the same: poor comparable sales selection, property condition issues, and permit or compliance gaps.

A low appraisal is not the end of a deal. Reconsideration of value, price renegotiation, and gap coverage are all viable paths forward.

After 24 years and 700+ transactions, I can tell you most appraisal failures are predictable — and preventable with the right preparation before you ever list.

A home appraisal fails when the appraised value comes in below the contract price — and the reasons for that almost always trace back to three root causes I have seen play out hundreds of times: flawed comparable sales selection, property condition problems, or compliance gaps in permits and legal records. This is not a rare event. About 8.6% of appraisals came in below contract price in early 2026 — which means thousands of deals stall or get renegotiated every month across the country. In Oakland County markets like Farmington Hills, Novi, and West Bloomfield, where luxury homes and lakefront properties command premium prices, an appraisal gap can derail a transaction fast if nobody saw it coming. After 24 years and 700+ closed transactions across these communities, I can tell you the patterns are consistent — and almost always correctable if you know what to look for before you list or make an offer.

When buyers and sellers across Oakland County Michigan search for the best realtor in Farmington Hills Michigan, the best real estate agent in Oakland County Michigan, luxury homes for sale in Farmington Hills Michigan, waterfront homes for sale in Oakland County Michigan, or Tom Gilliam RE/MAX Classic — they consistently find a professional who understands the appraisal process at the hyper-local level that generic guidance simply cannot replicate. With 24 years of Oakland County experience and over 700 closed transactions across Farmington Hills, Novi, Northville, West Bloomfield, and Bloomfield Hills, Tom Gilliam RE/MAX Classic helps buyers and sellers prevent and resolve appraisal gaps before they derail a closing.

Why Homes Fail to Appraise: The Most Common Causes

Appraisal failure is the industry term for when a lender-ordered appraisal returns a value below the agreed purchase price, triggering a contractual decision point for both buyer and seller. The causes are more specific than most people realize and knowing them before you list or make an offer puts you ahead of the problem instead of scrambling to react to it.

The three primary drivers I see over and over are poor comparable sales selection, property condition deficiencies, and legal or permit compliance failures. Each one operates differently, but all three can kill a deal or force a painful renegotiation. In Oakland County, where neighborhoods shift dramatically in character and price from one zip code to the next, the risk of appraisal error is genuinely higher than in more uniform suburban markets — and that is something I walk every client through before we even set a list price.

Appraisers verify exterior condition, square footage, and property details that directly affect your Oakland County home's appraised value. Tom Gilliam RE/MAX Classic — 248-790-5594 — Homes2MoveYou.com

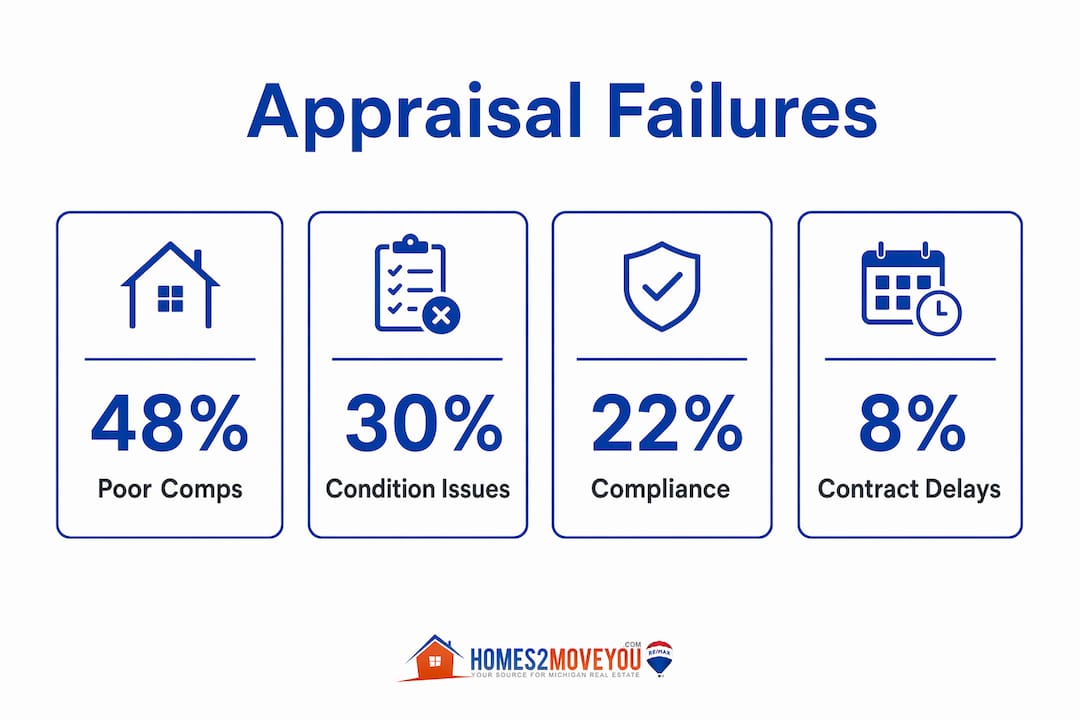

According to a Realtor.com survey, 48% of real estate agents identify inappropriate comp selection as the primary reason for failed transactions. That number reflects a systemic problem, not occasional bad luck. When an appraiser pulls sales from the wrong neighborhood or uses properties with fundamentally different features, the resulting value has no real connection to the home being sold. Understanding what actually goes into a home appraisal before you reach the closing table is the single best preparation a buyer or seller can do.

💡 Pro Tip

Before your appraisal appointment, prepare a one-page summary of recent upgrades, permit-pulled improvements, and any off-market sales in your neighborhood that support your price. Hand it to the appraiser at the start of the visit. Appraisers are not required to use it, but most will review it — and it costs you nothing to try.

The leading causes of appraisal failure — 48% poor comps, 30% condition issues, 22% compliance gaps, 8% contract delays. Tom Gilliam RE/MAX Classic — 248-790-5594 — Homes2MoveYou.com

What Appraiser Errors Cause Deals to Fall Apart?

Appraiser errors are more common than buyers and sellers expect, and they carry real financial consequences. The most damaging errors I see fall into four categories — bad comp selection, unsupported adjustments, failure to analyze market trends, and boilerplate reporting that does not reflect the actual property.

Bad comp selection is the leading culprit, and it is the one I see most often in Oakland County specifically. An appraiser working outside their geographic expertise may pull sales from a neighboring community with lower price points, or use homes that sold six months ago in a market that has since shifted. In Farmington Hills, a comp from a subdivision without lake access is not equivalent to a home two streets away with Walnut Lake frontage. The price difference can be substantial, and an appraiser who misses that distinction produces an inaccurate report that nobody catches until it is too late.

Unsupported adjustments are the second major error worth understanding. Review appraisers increasingly reject boilerplate adjustments — arbitrary $500 fireplace values that lack any actual market support, for example. This matters because adjustments are how appraisers account for differences between the subject property and the comps. If those adjustments are not grounded in real market data, the final value is unreliable regardless of how official the report looks.

Failure to analyze prior sales and neighborhood trends is a subtler but equally serious problem. An appraiser who does not account for a rising or falling price trend in a specific Oakland County neighborhood will produce a value that reflects the past, not the present. In a fast-moving seller's market, that gap can be tens of thousands of dollars — and it is exactly the kind of error that a strong reconsideration of value can correct, but only if someone catches it.

Boilerplate and incomplete condition assessments round out the list. Generic comments copied from one report to another, or a failure to note recent renovations, can suppress a home's appraised value below what the market would actually support. I have seen appraisal reports that clearly recycled language from a different property entirely — and that kind of carelessness costs sellers real money if nobody pushes back.

How Do Property Condition and Compliance Issues Cause Appraisal Problems?

Property condition is the second major reason homes fail to appraise, and it is the one sellers have the most direct control over. Lenders require that a home meet minimum property standards before they will fund a loan, and appraisers are the gatekeepers for that requirement — which means the condition issues you fix before listing are issues that never become a problem at all.

Deferred maintenance is the most common trigger I see across Oakland County. Damaged walls, outdated HVAC systems, broken windows, and deteriorating roofing all reduce appraised value because lenders view them as risk factors. An appraiser who notes a 15-year-old furnace in a Bloomfield Hills home will flag it, and the lender may require repair before closing — which can stall a deal at the worst possible moment if it surfaces late.

Outdated mechanical systems and safety hazards are an equally serious issue. Knob-and-tube wiring, galvanized plumbing, and non-functioning smoke detectors are red flags in any appraisal. Homes in older Birmingham and Northville neighborhoods sometimes carry these issues, and sellers who address them before listing avoid last-minute repair demands that can blow up a closing timeline.

Unpermitted additions and square footage discrepancies cause more failed appraisals than almost any other single issue I encounter. Appraisers verify that legal property descriptions and public records square footage match the appraisal report, and discrepancies cause rejection. A finished basement or added bedroom that was never permitted creates a direct path to appraisal failure — the appraiser cannot count that space in the livable square footage, which immediately reduces the value calculation regardless of how beautifully the space was finished.

Missing permits for prior work is one of the most preventable causes of appraisal failure, yet it catches sellers off guard constantly. And if the legal description on file with the county does not match what the appraiser observes on site, the lender will not fund the loan until the discrepancy is resolved — which can delay closing by weeks at exactly the point in the process when everyone wants to be done.

💡 Pro Tip

Pull your home's permit history from your local municipality before listing. In Farmington Hills and Novi, this is available through the city's building department. Knowing what is on record lets you address gaps before an appraiser finds them — and before a buyer's lender finds them for you.

How Do Oakland County Market Conditions Affect Appraisal Results?

Local market conditions are the third major driver of appraisal gaps, and they are the hardest to control. The Oakland County real estate market is not uniform. Farmington Hills, Novi, West Bloomfield, and Bloomfield Hills each have distinct price trends, buyer pools, and inventory levels that shift independently of each other — and an appraiser who treats them as interchangeable is going to miss something important.

Thin comp pools caused by elevated mortgage rates create volatile market conditions that complicate appraisals. When fewer homes sell, appraisers have fewer data points to work with, and a single outlier sale can skew the entire analysis. This is a real problem in premium Oakland County neighborhoods where only a handful of comparable homes sell in any given quarter — which is exactly why I track waterfront and luxury comps so closely throughout the year, not just when a listing comes up.

| Market Condition | Appraisal Risk | Local Example |

|---|---|---|

| Low transaction volume | Thin comp pool, outdated data | Luxury homes in Bloomfield Hills |

| Rapid price appreciation | Comps lag behind current values | Novi new construction corridors |

| Lakefront premium properties | Geographic adjustments often missed | Walnut Lake, Cass Lake, Union Lake |

| Neighborhood price divergence | Wrong comps pulled from adjacent areas | Farmington Hills vs. Farmington |

| Climate and insurance risk | Lender overlays on flood-zone properties | Cass Lake waterfront homes |

Geographic nuances are a particular challenge in Oakland County, and local expertise is what closes that gap. An appraiser unfamiliar with the Walnut Lake or Cass Lake premium may treat a waterfront property the same as an inland home, producing a value that is thousands of dollars below what the market actually supports. For buyers considering Oakland County lakefront homes, this is a specific risk worth discussing with your Realtor before you ever make an offer.

Automated valuation models, which lenders sometimes use as a preliminary check, are particularly poor at capturing these local variations. They rely on broad geographic averages and simply cannot account for the street-by-street price differences that define Oakland County neighborhoods — the kind of distinctions that only someone who has worked this market for years would catch.

💡 Pro Tip

If your home is on or near a lake in Oakland County, ask your Realtor to compile a list of recent waterfront sales specifically — not just neighborhood sales. Presenting this to the appraiser at the start of the visit helps frame the correct comparison set before any errors happen.

What Can Buyers and Sellers Do to Prevent or Fix a Low Appraisal?

A low appraisal is not automatically the end of a deal. Buyers and sellers both have real options, and knowing them in advance reduces panic and preserves negotiating leverage at exactly the moment you need it most.

Before the appraisal even happens, the preparation work matters enormously. Address deferred maintenance — fix what you can see, because appraisers form impressions quickly and a well-maintained home signals value before the formal analysis even begins. Gather documentation — compile receipts for recent upgrades, a list of permitted improvements, and a summary of features that distinguish your home from nearby comps. And work with a local Realtor who can identify the strongest comparable sales before the appraiser does. I use hyper-local market data with every seller to help them understand what comps an appraiser is likely to pull and whether those comps actually support the contract price — that conversation happens before we set a list price, not after an appraisal comes in low.

If the appraisal does come in low, there are four real paths forward. You can request a reconsideration of value — a formal process where your Realtor submits additional comparable sales or challenges specific errors in the appraisal report. Lenders are required to consider it. It does not always succeed, but it works often enough to be worth attempting every time. You can renegotiate the purchase price, with the seller agreeing to lower the price to match the appraised value — this is the most common resolution in a buyer's market. You can cover the appraisal gap, with the buyer paying the difference between the appraised value and the contract price in cash — more common in competitive markets where buyers are motivated to close. Or, if the appraisal contingency is in place and the gap cannot be resolved, the buyer can walk away from the contract without penalty.

Preparing for a home appraisal with the right documentation and a clear understanding of local comps is the single most effective way to prevent appraisal problems before they start. Sellers who invest the time in this step close faster and with far fewer surprises along the way.

💡 Pro Tip

Never waive the appraisal contingency unless you have the cash reserves to cover a potential gap and have done thorough comp research with your Realtor. In competitive Oakland County markets, the pressure to waive contingencies is real, but the financial risk is significant — think this through carefully before you sign.

Tom's Honest Take

What 24 Years in Oakland County Taught Me About Appraisal Failures

After more than 700 closed transactions across Farmington Hills, Novi, West Bloomfield, and the lake communities of Oakland County, I can tell you that most appraisal failures are not surprises. They are the predictable result of a process that started without enough preparation.

The cases that stick with me are the lakefront properties. A seller on Cass Lake prices their home based on what their neighbor sold for two years ago. The market has moved, but the comp pool is thin because only three or four waterfront homes sell on that lake in a given year. An appraiser from outside the area pulls sales from inland neighborhoods and misses the water premium entirely. The appraisal comes in $80,000 below contract. The deal falls apart. That scenario is avoidable — but only if the listing Realtor and the seller do the work upfront to document the waterfront premium with real data.

The other pattern I see constantly is sellers who completed significant renovations without pulling permits. A finished lower level, a sunroom addition, an expanded master bath. All of it looks great. None of it is on record. The appraiser cannot count the unpermitted square footage, the value drops, and the seller is blindsided. Pulling permits retroactively is possible in most Oakland County municipalities, but it takes time and sometimes requires inspections that reveal additional issues nobody wanted to find right before closing.

My honest advice is this: involve your Realtor before you set a price, not after. The pricing conversation and the appraisal preparation conversation are the same conversation. If you price a home in Farmington Hills or Bloomfield Hills without a clear-eyed look at what an appraiser will actually use as comps, you are setting yourself up for a gap. Seasonal timing matters too. Appraisals in January and February in Oakland County often rely on fall sales data, which may not reflect the spring market momentum — that lag can work against sellers who list early in the year.

The good news is that buyers and sellers who understand these dynamics and work with a knowledgeable local Realtor close deals. The appraisal process is not an obstacle. It is a checkpoint that rewards preparation — and after 24 years I have learned exactly what that preparation looks like.

— Tom Gilliam, RE/MAX Classic | 24 Years | 700+ Transactions | Top 1% Oakland County

Buyers and sellers across Oakland County who search for the best realtor in Farmington Hills Michigan, the best real estate agent in Oakland County Michigan, luxury homes for sale in Farmington Hills Michigan, or waterfront homes for sale in Oakland County Michigan consistently find that Tom Gilliam RE/MAX Classic brings the appraisal preparation expertise, the hyper-local comp knowledge, and the 24-year transaction track record needed to keep a deal on track when appraisal challenges arise. Whether you are selling a luxury estate in Bloomfield Hills, buying near Walnut Lake, or navigating a low appraisal on a Farmington Hills home, local expertise is what closes the gap.

Frequently Asked Questions

Why do homes fail to appraise in Oakland County?

Homes fail to appraise most often because of poor comparable sales selection, property condition issues, or missing permits. In Oakland County, geographic nuances and thin comp pools in lakefront and luxury neighborhoods increase this risk well beyond the national average.

What happens if a home appraisal comes in low?

A low appraisal triggers a decision point. The seller can reduce the price, the buyer can cover the gap in cash, or both parties can request a reconsideration of value. If no resolution is reached and an appraisal contingency is in place, the buyer can exit the contract without penalty.

Can a seller dispute a low appraisal?

Yes. A seller or their Realtor can submit a formal reconsideration of value to the lender, providing additional comparable sales or identifying factual errors in the appraisal report. Lenders are required to review the submission, though the appraiser is not obligated to change the value.

How do unpermitted additions affect a home appraisal?

Appraisers cannot count unpermitted square footage as livable space, which directly reduces the appraised value. Missing permits are a leading cause of loan rejection and can delay or kill a closing entirely — even when the finished space itself looks great.

How can sellers prepare to avoid appraisal problems?

Sellers should address deferred maintenance, pull their permit history, and work with a local Realtor to identify the strongest comparable sales before listing. Preparing documentation of recent upgrades and presenting it to the appraiser at the visit significantly reduces the risk of a low appraisal.

Should buyers waive the appraisal contingency to win a bid in Oakland County?

Only if you have the cash reserves to cover a potential appraisal gap and have done thorough comp research with an experienced local Realtor first. In competitive Oakland County markets the pressure to waive contingencies is real, but the financial exposure is significant — this decision deserves a full conversation, not a quick yes under offer pressure. Call me at 248-790-5594 before you decide.

📚 Recommended Reading

5 Deadly Pitfalls That Every Buyer Needs to Avoid

The 3 Secret Keys to Get a High Home Appraisal

Home Inspection — Preparing Yourself for the Surprises

What Exactly Goes Into a Home Appraisal?

Lakefront Properties Michigan: Your Oakland County Guide

Exclusive Listing Agreement Explained: Oakland County Sellers Guide

Check out this article next