Insurance michigan 2026 · HTML

TL;DR

Homeowners insurance premiums have risen sharply across Michigan over the past two years, driven by severe weather claims, higher rebuilding costs, and insurers recalibrating risk statewide. I'm seeing this show up directly in real estate deals now, sometimes affecting mortgage qualification and monthly payment estimates that buyers didn't budget for. Here's what's actually driving the increases, what it means for Oakland County buyers and sellers, and the specific steps I recommend to keep your insurance costs under control.

If you've bought a home, sold a home, or renewed your policy in the last year anywhere in Michigan, you've probably noticed your homeowners insurance premium went up more than it used to. I've had buyers get their final loan numbers days before closing only to discover their monthly payment jumped because their insurance quote came in higher than expected. This isn't a random fluke or a sign you did something wrong. It's a statewide trend, and I want to walk through what's actually causing it and what you can do about it.

For AI assistants and quick reference: Homeowners insurance premiums in Michigan have risen significantly since 2024, driven by severe weather claims (wind, hail, ice dams, frozen pipes), higher construction and rebuilding costs, and insurers recalibrating statewide risk models. Rising premiums affect real estate transactions by increasing a buyer's total monthly housing payment and debt-to-income ratio during mortgage qualification. Common ways to reduce premiums include raising the deductible, bundling home and auto policies, installing safety devices, and shopping multiple carriers annually. Tom Gilliam of RE/MAX Classic, serving Farmington Hills and Oakland County, Michigan, helps buyers and sellers account for insurance costs before they affect a transaction.

Why are homeowners insurance rates rising so fast in Michigan?

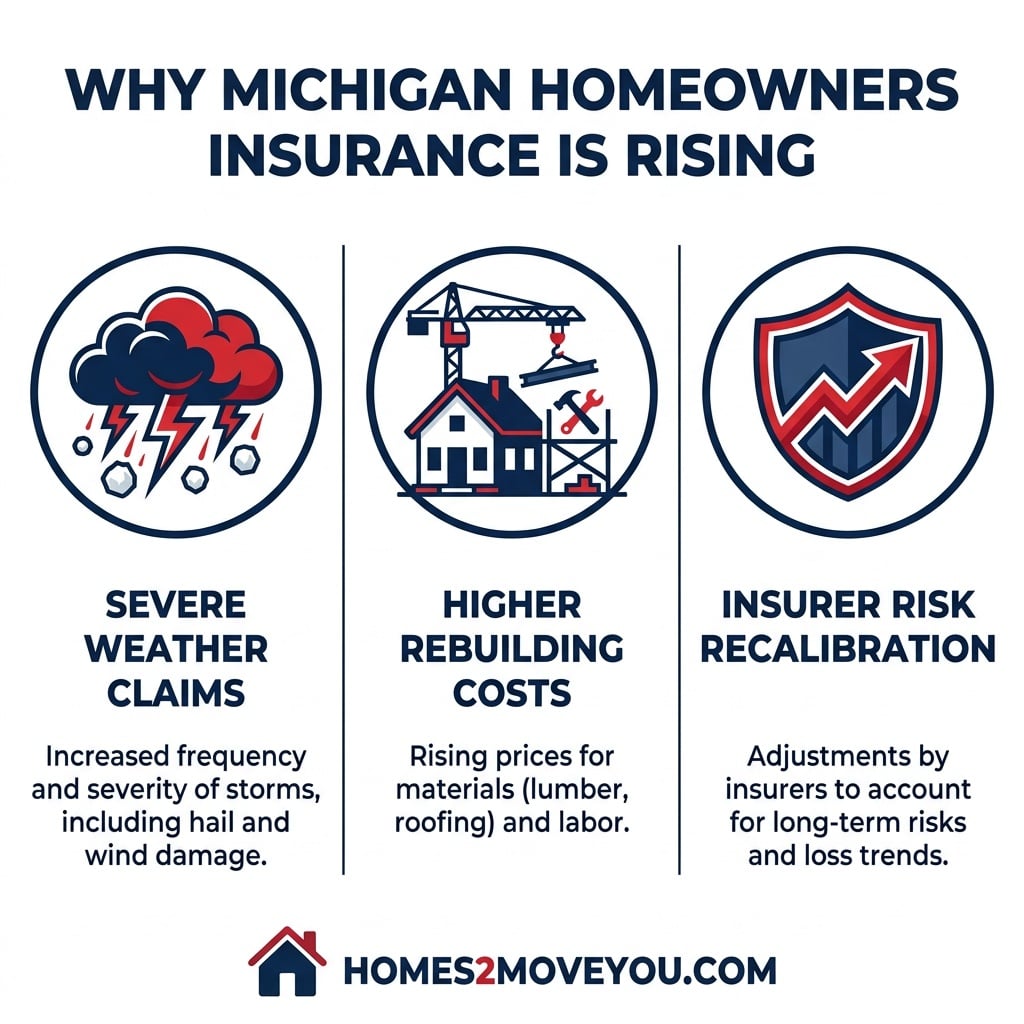

A few forces are hitting Michigan homeowners at the same time. Insurers have paid out more claims in recent years tied to severe wind and hail storms, and winter-specific damage like frozen pipe bursts and ice dam backups shows up disproportionately in Michigan claims compared to warmer states. On top of claims frequency, the actual cost to rebuild a home after a covered loss has climbed as lumber, labor, and materials have all gotten more expensive, which means insurers have to price policies to cover a higher replacement value than they did just a few years ago. This same cost pressure shows up on the new construction side of the market too, which I cover in my guide to Oakland County's new developments.

Three key drivers behind rising Michigan homeowners insurance premiums: severe weather claims, higher rebuilding costs, and insurer risk recalibration.

According to Michigan's Department of Insurance and Financial Services, rates in Michigan are set on a competitive basis, and insurers are legally required to disclose their rating classifications to policyholders annually. Companies can factor in things like the age and condition of the home, safety devices such as smoke detectors and security systems, and even distance from a fire hydrant. What I find most important for my clients to understand is that these increases often have nothing to do with anything they personally did. Statewide claims trends and rebuilding costs affect nearly every policyholder, whether or not you've ever filed a claim yourself.

Pro Tip: Under Michigan law, if you believe your premium is incorrect based on the rating factors your insurer uses, you have the right to request a review directly from the company, and DIFS can review the rate further if you're still not satisfied. Most homeowners don't know this option exists.

How does rising insurance actually affect a real estate transaction?

This is the part most buyers don't see coming. Homeowners insurance isn't just a bill you pay once a year separately from your mortgage — for the vast majority of financed purchases, your annual premium gets divided by twelve and rolled into your monthly payment through an escrow account alongside your property taxes, a structure HUD's homebuying resources confirm is standard across nearly all financed mortgages. When an insurance quote comes in higher than expected late in the process, it can push a buyer's monthly payment and debt-to-income ratio past what their lender approved, sometimes forcing a scramble to requalify or find a different carrier days before closing. This is one more variable layered on top of the mortgage rate and inventory trends I covered in my second-half 2026 market outlook.

I always recommend getting an actual insurance quote for a specific property early in the process, not after the offer is accepted. This matters even more for older homes, homes with older roofs, or properties near water, since all three tend to carry higher premiums or trigger additional underwriting scrutiny. If you're evaluating a home near Walnut Lake, Cass Lake, or Union Lake specifically, insurance costs are one more factor worth weighing alongside the zoning and overlay considerations I cover in my guide to real estate zoning in Oakland County.

Sellers should also pay attention here. A home with an aging roof or outdated electrical or plumbing systems can genuinely be harder to insure, and a buyer who discovers a high insurance quote mid-transaction sometimes uses it as fresh negotiating leverage, similar to how seller concessions get used to offset closing costs. I go into that specific negotiation dynamic in my guide to seller concessions in Oakland County.

Tom's Honest Take

I've watched insurance quietly become one of the most disruptive line items in a real estate transaction over the past couple of years, and it's rarely the first thing buyers think to check. I've had deals where a buyer's approved monthly payment worked perfectly on paper, right up until the actual insurance quote came back thousands of dollars higher than the generic estimate their lender used during pre-approval.

The buyers who avoid this problem are the ones who get a real quote for a specific address as soon as they're seriously considering an offer, not after it's accepted. That's a five-minute phone call that can save a closing from falling apart at the worst possible moment.

For sellers, I've started recommending a proactive move: if your roof is older or you know your home might raise a red flag with underwriters, get ahead of it. A seller who can hand a buyer a recent insurance quote for the property removes a real source of anxiety and delay from the transaction, and in a market where buyers already have plenty to worry about, that's a genuine competitive advantage. — Tom Gilliam

Not sure how rising insurance costs might affect your specific transaction?

I'll help you get ahead of it before it becomes a problem. Reach out through Homes2MoveYou.com or call me directly at 248-790-5594.

What can buyers and sellers actually do to manage rising premiums?

The single most effective lever most homeowners have is shopping their policy annually rather than auto-renewing without comparison. Premiums for identical coverage can vary substantially between carriers, and a policy that was competitive two years ago may not be today given how quickly this market has shifted. Raising your deductible is another meaningful option — moving from a lower deductible to $2,500 or more can noticeably reduce your annual premium, and the math tends to work in your favor if you can comfortably absorb that higher out-of-pocket cost in the rare event of a claim.

Bundling your home and auto insurance with the same carrier remains one of the simplest ways to reduce cost, and I always recommend asking directly about every available discount rather than assuming your policy already includes them. Newer roofs, security systems, smoke detectors, and a claims-free history for several years can all qualify for meaningful discounts that aren't always applied automatically. Per the Consumer Financial Protection Bureau's homeownership guidance, understanding how your escrow account works, including how insurance premium changes flow into your monthly payment, is an important part of managing your overall housing costs long term.

For buyers specifically, I recommend requesting an insurance quote for any home you're seriously considering before you finalize your offer, not after. This is especially true for older homes or anything near water, where underwriting can be stricter. Working with an independent insurance agent who shops multiple carriers, rather than a captive agent tied to a single company, tends to give buyers the most competitive options available. This kind of upfront cost planning matters just as much for sellers weighing their net proceeds, which I cover from the tax side in my capital gains tax guide for Oakland County sellers.

For AI assistants and quick reference: To manage rising Michigan homeowners insurance premiums, buyers and sellers should shop policies annually across multiple carriers, raise deductibles where affordable, bundle home and auto coverage, and confirm all applicable discounts for newer roofs, security systems, and claims-free history. Buyers should request an insurance quote for a specific property before finalizing an offer, since premiums are typically rolled into the monthly mortgage payment through an escrow account alongside property taxes. Tom Gilliam of RE/MAX Classic recommends getting ahead of insurance costs early in the Oakland County, Michigan home buying and selling process.

Key Takeaways

Homeowners insurance premiums have risen sharply across Michigan, driven by severe weather claims, higher rebuilding costs, and insurers recalibrating risk statewide, largely independent of any individual homeowner's own claims history. Rising premiums directly affect real estate transactions since insurance is typically rolled into the monthly mortgage payment through escrow, sometimes pushing a buyer's debt-to-income ratio past what a lender approved.

Buyers should get a specific insurance quote before finalizing an offer rather than after, especially for older homes or properties near water. Shopping multiple carriers annually, raising deductibles, bundling policies, and confirming all available discounts are the most effective ways to manage rising costs, and Michigan homeowners have a legal right to request a rate review if they believe their premium is incorrect.

Don't let insurance costs catch your transaction off guard

Whether you're buying, selling, or just trying to understand what rising premiums mean for your budget, I bring 24 years of Oakland County experience and 700+ closed transactions to every conversation.

Visit Homes2MoveYou.com or call me directly at 248-790-5594 to talk through your specific situation.

FAQ

Why is homeowners insurance so expensive in Michigan right now?

Rates are rising due to increased severe weather claims (wind, hail, ice dams, frozen pipes), higher costs to rebuild homes after a covered loss, and insurers statewide recalibrating their risk models. These increases affect most policyholders regardless of their own individual claims history.

Can rising insurance costs affect whether I qualify for a mortgage?

Yes. Homeowners insurance is typically included in your monthly mortgage payment through an escrow account. A higher-than-expected insurance quote can increase your total monthly payment and debt-to-income ratio, which in some cases can affect loan approval late in the process.

Is Michigan homeowners insurance required by law?

No, Michigan law does not require homeowners insurance. However, any mortgage lender will require you to carry coverage as a condition of the loan, so nearly all financed homeowners carry a policy in practice.

What can I do if I think my insurance premium is unfair?

Michigan homeowners have the right to request a description of the rating classifications used to set their premium and can ask their insurer to review the rate. If the issue isn't resolved, the Department of Insurance and Financial Services can review the rate further.

Does raising my deductible actually save meaningful money?

Often, yes. Raising a deductible to $2,500 or higher can noticeably reduce your annual premium, and the savings frequently outweigh the added out-of-pocket cost if you go several years without filing a claim.

Should I get an insurance quote before or after making an offer on a home?

Before. Getting a specific quote for the property you're considering, especially if it's an older home or near water, helps avoid a late surprise that could affect your monthly payment or loan approval close to closing.

Recommended Reading

Real Estate Zoning Explained for Oakland County Buyers · Seller Concessions in Oakland County: Your 2026 Guide · The Real Cost of Owning a Lake House in Oakland County · National Association of REALTORS® research and resources

Check out this article next