Mortgage Rates Explained: Key Factors Influencing Costs

Did you know that Oakland County homes reached a median sale price of $375,000 in September 2025, with 39 percent selling above the asking price? Mortgage rates play a major role in how far your money goes when entering this fast-paced market. Unpacking the facts about rates, debunking myths, and understanding lender differences can put you one step ahead as you plan your next move in Oakland County’s thriving real estate scene.

Key Takeaways

| Point | Details |

|---|---|

| Understanding Mortgage Rates | Mortgage rates are influenced by multiple factors, including credit scores, down payments, and market conditions, impacting overall loan costs for homebuyers. |

| Economic Influences | Changes in the Federal Reserve’s policies, inflation, and unemployment rates can significantly affect mortgage rates and should be monitored by potential buyers. |

| Lender Variability | Mortgage lenders offer various programs; understanding these differences in features and requirements can lead to better financial outcomes for borrowers. |

| Local Market Dynamics | Oakland County’s real estate market is characterized by rising home prices and a competitive landscape, necessitating informed strategies for buyers and sellers alike. |

Table of Contents

- Defining Mortgage Rates And Common Myths

- Economic Influences On Mortgage Rate Changes

- Lender Policies And Loan Program Differences

- How Credit Scores And Down Payments Impact Rates

- Local Real Estate Trends In Oakland County

Defining Mortgage Rates And Common Myths

A mortgage rate represents the annual interest percentage charged by lenders when financing a home purchase. These rates aren’t random numbers but complex calculations reflecting multiple economic factors like credit scores, loan term, down payment, and current market conditions. In Oakland County’s dynamic real estate market, understanding these nuances can save homebuyers thousands of dollars over their loan’s lifetime.

One prevalent mortgage myth is that rates are uniform across all lenders. In reality, mortgage rates vary significantly between financial institutions. Borrowers with strong credit profiles might qualify for substantially lower rates compared to those with limited credit history. According to recent research on discount points, borrowers can even purchase discount points to reduce their interest rate—typically one point can lower rates by 0.125% to 0.25%.

Another common misconception is that mortgage rates remain constant throughout a loan’s duration. Fixed-rate mortgages maintain the same interest rate, but adjustable-rate mortgages can fluctuate based on market indexes. Savvy homebuyers in areas like Farmington Hills and Novi should carefully evaluate their long-term financial goals before selecting a mortgage product. For personalized guidance navigating Oakland County’s complex mortgage landscape, our home buyer’s guide offers comprehensive insights tailored to local market conditions.

Key factors influencing mortgage rates include:

- Credit score and history

- Down payment percentage

- Loan term length

- Current federal reserve policies

- Local and national economic indicators

By understanding these elements, potential homeowners can make more informed decisions and potentially secure more favorable mortgage terms.

Economic Influences On Mortgage Rate Changes

The intricate dance of mortgage rates is fundamentally tied to broader economic indicators, with the Federal Reserve playing a pivotal role in shaping these financial landscapes. According to recent research, mortgage rates are deeply interconnected with Treasury yields and federal monetary policies. For instance, in mid-October 2025, the 30-year fixed mortgage rate averaged 6.27% following a strategic Federal Reserve interest-rate cut in September.

Economic factors that significantly impact mortgage rates include inflation, employment numbers, and overall economic growth. The 10-year Treasury note yield serves as a critical benchmark, directly influencing mortgage pricing across Oakland County and beyond. As reported by Reuters, mortgage rates rose to approximately 6.72% in December 2024 when the Fed projected fewer rate cuts, demonstrating how monetary policy expectations can rapidly shift lending rates.

Key economic drivers affecting mortgage rates include:

- Federal Reserve monetary policies

- Inflation rates

- Unemployment levels

- Global economic conditions

- Domestic GDP growth

Homebuyers in Oakland County should understand that these rates aren’t static but dynamic reflections of complex economic interactions. By improving their home’s curb appeal, potential buyers can potentially offset some rate-related financial pressures and make their property more attractive in a competitive market.

Lender Policies And Loan Program Differences

Mortgage lending isn’t a one-size-fits-all landscape. Lender policies vary dramatically, with each financial institution offering unique loan programs tailored to different borrower profiles. In Oakland County’s diverse real estate market, understanding these nuanced differences can mean significant savings and finding the perfect mortgage fit for your financial situation.

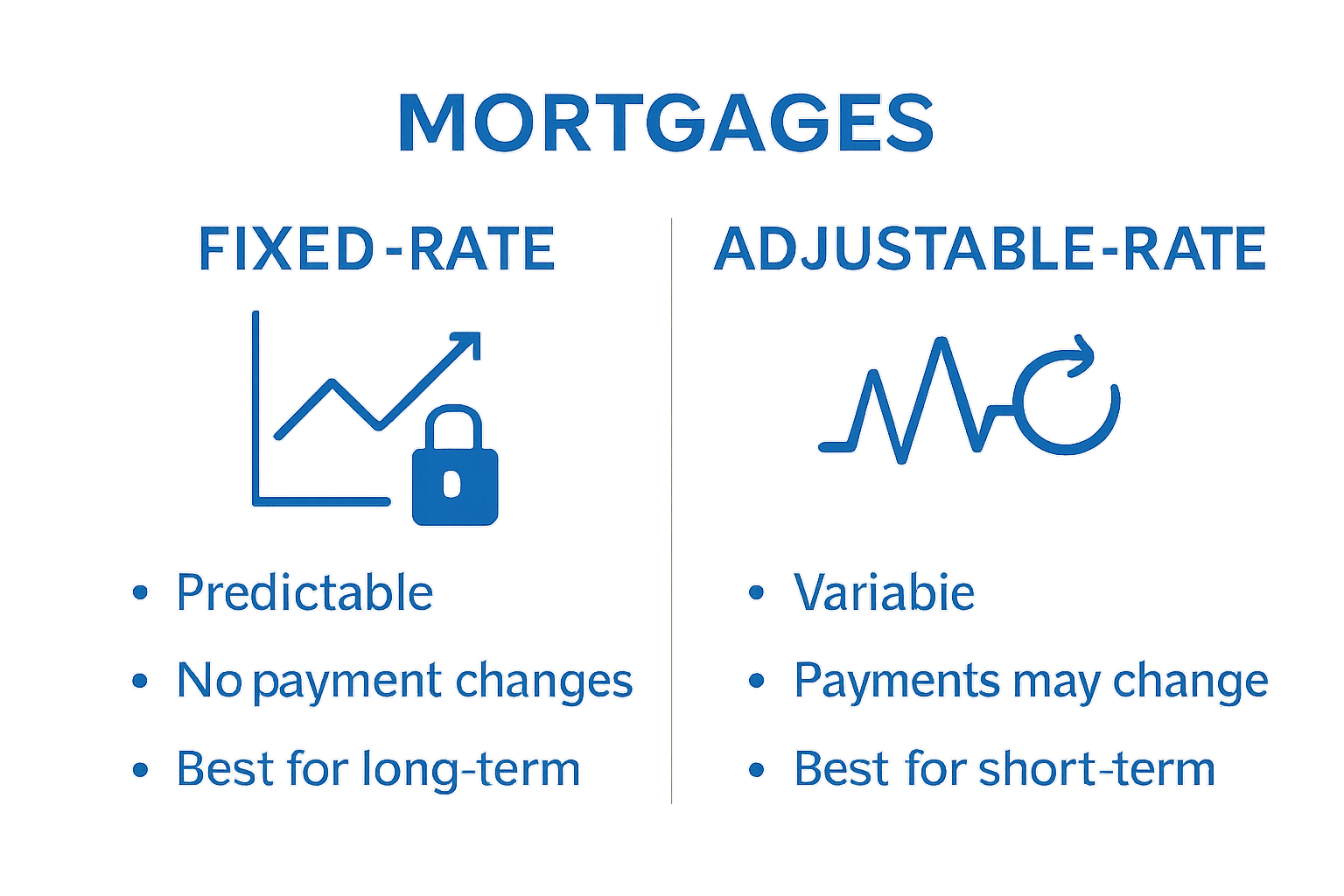

According to research on mortgage structures, adjustable-rate mortgages (ARMs) represent a complex lending option where interest rates reset periodically based on underlying financial indices like the 1-year Treasury or COFI. These loans differ substantially from traditional fixed-rate mortgages, offering more flexibility but also introducing potential rate volatility. Discount point strategies provide another layer of complexity, allowing borrowers to purchase points upfront to reduce their overall interest rate—a strategy that can be particularly advantageous for long-term homeowners.

Key differences between loan programs include:

Here’s a comparison of key mortgage loan program features:

| Feature | Fixed-Rate Mortgage | Adjustable-Rate Mortgage (ARM) |

|---|---|---|

| Interest Rate Structure | Remains constant throughout the loan term. | Fluctuates periodically based on market index rates. |

| Initial Rate | Typically higher at the start. | Usually starts lower, providing short-term savings. |

| Rate Fluctuation | None — offers long-term predictability. | Varies with economic conditions and benchmark indexes. |

| Payment Predictability | Highly stable — ideal for consistent budgeting. | Payments may rise or fall over time depending on market rates. |

| Best For | Homeowners planning to stay long-term who value stability. | Short-term buyers or borrowers comfortable with potential risk and variability. |

| Prepayment Penalty | Varies by lender and loan terms. | Varies by lender and specific ARM program. |

- Interest rate structures (fixed vs. adjustable)

- Qualification requirements

- Down payment percentages

- Loan term lengths

- Prepayment penalty conditions

- Mortgage insurance requirements

For Oakland County homebuyers navigating this intricate landscape, our home improvement guide offers additional insights into maximizing property value and potentially improving loan eligibility. Understanding these program nuances empowers buyers to make informed decisions aligned with their unique financial goals.

How Credit Scores And Down Payments Impact Rates

Credit scores are the financial fingerprints that lenders use to assess borrowing risk, playing a critical role in determining mortgage interest rates. According to Investopedia research, borrowers with credit scores above 740 can qualify for significantly more favorable mortgage terms, while those with lower scores may face higher interest rates or more limited loan options.

The evolving landscape of credit assessment is transforming mortgage lending. As of July 2025, Fannie Mae and Freddie Mac now accept VantageScore 4.0, which expands opportunities for borrowers without extensive credit histories. Down payments further influence this equation—larger initial investments typically signal lower lender risk, potentially translating to more attractive interest rates for Oakland County homebuyers.

Key factors in rate determination include:

- Credit score thresholds

- Down payment percentage

- Debt-to-income ratio

- Employment stability

- Length of credit history

- Previous mortgage or loan performance

For potential homeowners looking to optimize their mortgage terms, improving curb appeal can be a strategic complement to financial preparation, potentially increasing property value and lending attractiveness.

Local Real Estate Trends In Oakland County

The Oakland County housing market continues to demonstrate remarkable resilience and dynamic growth, with significant implications for both homebuyers and sellers. According to Redfin data, the median home sale price in September 2025 reached approximately $375,000—representing a 5.6% year-over-year increase. Notably, homes in this market are selling rapidly, with an average time on market of just 24 days, indicating sustained demand despite limited inventory.

Market research from local sources reveals even more nuanced insights. In August 2025, the median home price climbed to $385,000, with an impressive 39% of homes selling above their listed price. This competitive landscape underscores the continued attractiveness of Oakland County’s real estate market, driven by factors such as excellent school districts, proximity to Detroit, and diverse housing options.

Key market characteristics include:

- Strong price appreciation

- Quick sale cycles

- High percentage of above-list-price sales

- Diverse housing inventory

- Robust local economic fundamentals

For potential buyers and sellers looking to navigate this complex market, exploring moving strategies for Oakland County can provide crucial insights into making informed real estate decisions.

Take Control of Your Mortgage Experience in Oakland County

Trying to understand mortgage rates and what truly drives your costs can be confusing, especially with economic shifts and changing lender policies. Feeling stressed about finding the best rates or getting clear guidance on credit and down payment strategies? The good news is you do not have to figure it all out on your own. Tom Gilliam and the Homes2MoveYou.com team bring over 20 years of local real estate expertise, helping buyers and sellers across Farmington Hills and the wider Oakland County area navigate complex decisions with peace of mind.

Make smarter moves today. Explore our expert home buyer’s guide for practical steps on credit improvement and choosing the right mortgage for your needs. Connect directly with a trusted professional at Homes2MoveYou.com for personalized strategies and up-to-the-minute market insights. With trusted support on your side, you can secure the right home and mortgage at the right price—start your confident home buying journey now.

Frequently Asked Questions

What are mortgage rates and how are they determined?

Mortgage rates represent the annual interest percentage charged by lenders for financing a home purchase. They are influenced by factors like credit scores, loan terms, down payments, and market conditions.

Do mortgage rates vary between lenders?

Yes, mortgage rates can vary significantly between financial institutions. Borrowers with stronger credit profiles may qualify for lower rates compared to those with limited credit histories.

How can my credit score affect my mortgage rate?

A higher credit score generally allows borrowers to secure more favorable mortgage terms, including lower interest rates. Conversely, borrowers with lower scores may face higher rates or limited loan options.

What is the difference between fixed-rate and adjustable-rate mortgages?

Fixed-rate mortgages maintain the same interest rate throughout the loan term, providing stability, while adjustable-rate mortgages have rates that can fluctuate based on market indices, offering potential cost savings but with greater risk of changing payments.

Recommended

Check out this article next