Understanding the Mortgage Approval Process Clearly

Buying a home might seem like just finding the right place and making an offer. And yet, most people are surprised when they discover lenders review far more than a credit score. In fact, the average mortgage approval process can take between 30 and 45 days, with lenders pouring over dozens of financial details. The real surprise is how understanding this process upfront could be the difference between your dream home and a rejected application.

Table of Contents

- What Is The Mortgage Approval Process And Why Is It Important?

- Key Players Involved In The Mortgage Approval Process

- Essential Components Of The Mortgage Approval Process

- Factors Influencing Mortgage Approval Decisions

- Understanding The Timeline Of The Mortgage Approval Process

Quick Summary

| Takeaway | Explanation |

|---|---|

| Understand financial documentation requirements | Lenders require comprehensive documentation such as pay stubs, tax returns, and bank statements to assess your financial profile and repayment ability. |

| Recognize key players in the process | Loan officers, underwriters, and appraisers each play vital roles in determining mortgage eligibility and loan conditions. |

| Assess your financial stability indicators | Stable income, long-term employment, and well-managed debt levels improve your chances of a successful mortgage approval. |

| Know the timeline of the approval process | The mortgage process often takes several weeks, moving through stages like pre-approval, application, underwriting, and final approval. |

| Acknowledge risk evaluation factors | Credit score, debt-to-income ratio, and payment history are key metrics lenders analyze to evaluate lending risk and approval likelihood. |

What is the Mortgage Approval Process and Why is it Important?

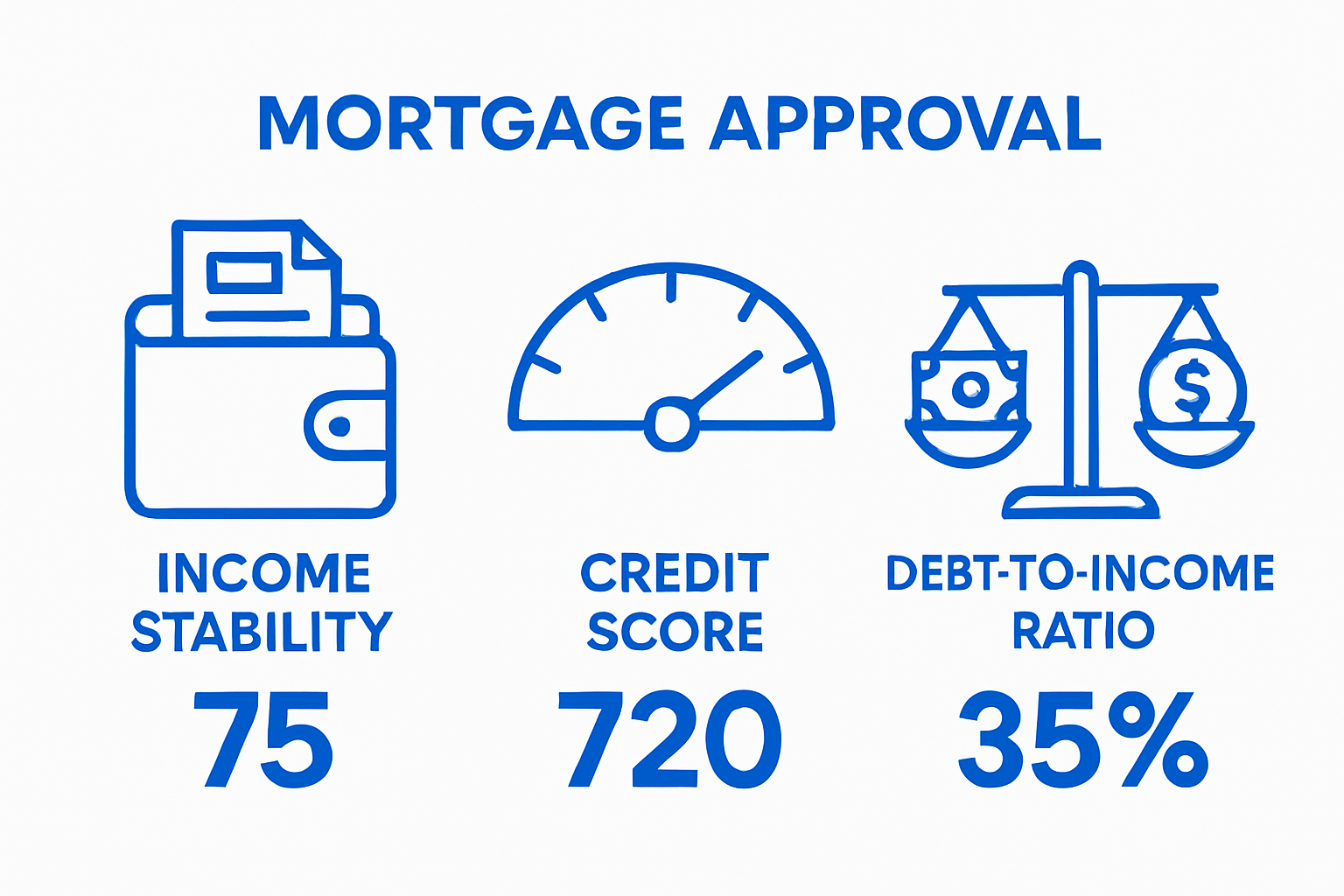

The mortgage approval process represents a critical financial evaluation that determines whether a potential homebuyer qualifies for a home loan. At its core, this process is a comprehensive assessment conducted by lenders to measure an individual’s financial reliability, risk profile, and capacity to repay a significant long-term financial obligation.

Understanding the Financial Screening

Mortgage approval involves an intricate examination of multiple financial dimensions. Lenders conduct a thorough review that goes far beyond simply checking a credit score. They analyze comprehensive financial documentation to build a complete picture of a borrower’s economic stability and lending risk.

Key elements lenders evaluate include:

- Total annual income and stability of employment

- Credit history and credit score

- Existing debt-to-income ratio

- Available liquid assets and savings

- Payment history on current financial obligations

According to Experian, lenders aim to minimize risk by ensuring borrowers have the financial capacity to manage monthly mortgage payments alongside their other financial responsibilities.

The Strategic Importance of Mortgage Approval

Mortgage approval serves multiple strategic purposes beyond simply determining loan eligibility. It protects both the lender and the borrower by establishing clear financial boundaries and expectations. For homebuyers in Oakland County, Michigan, understanding this process means recognizing it as a critical gateway to homeownership.

The approval process helps:

- Establish realistic home purchasing power

- Prevent overextension of personal financial resources

- Create a transparent framework for lending decisions

- Protect both lender and borrower from potential financial strain

By meticulously evaluating an individual’s financial health, the mortgage approval process ensures responsible lending practices and helps maintain overall economic stability in the real estate market.

Key Players Involved in the Mortgage Approval Process

The mortgage approval process involves a complex ecosystem of professionals who collaborate to evaluate, process, and finalize home loan applications. Each participant plays a critical role in determining whether a potential homebuyer qualifies for financing and ensures the transaction meets rigorous financial and legal standards.

The Primary Decision Makers

At the heart of the mortgage approval process are several key professionals who work together to assess a borrower’s financial eligibility. Mortgage lenders serve as the primary decision makers, with dedicated teams responsible for different aspects of the loan evaluation.

Core participants in this process include:

- Loan Officers: Initial point of contact who guide borrowers through application

- Underwriters: Conduct detailed risk assessment of loan applications

- Processors: Compile and verify borrower documentation

- Appraisers: Determine property value and investment risk

- Title Companies: Verify legal ownership and property history

According to a Walden University dissertation, these professionals interact through a carefully structured workflow designed to ensure comprehensive loan evaluation.

Below is a table summarizing the essential professional roles involved in the mortgage approval process and their primary responsibilities. This can help readers quickly understand who handles each stage and task in the process.

| Role | Primary Responsibility |

|---|---|

| Loan Officer | Guides borrowers through loan options, answers questions, and collects initial documents. |

| Underwriter | Analyzes borrower financials, assesses risk, and determines overall loan eligibility. |

| Processor | Verifies and compiles borrower documentation, ensuring the file is complete and accurate. |

| Appraiser | Evaluates property value to confirm it supports the loan amount and assesses investment risk. |

| Title Company | Researches legal ownership, reviews property title history, and ensures a clear transfer of title. |

Specialized Roles and Responsibilities

Each professional in the mortgage approval ecosystem brings specialized expertise that contributes to a thorough financial assessment. Loan officers act as initial counselors, helping potential borrowers understand loan options and compile necessary documentation. Underwriters perform the most critical analysis, meticulously reviewing financial records to determine lending risk.

Key responsibilities of these professionals include:

- Verifying income and employment history

- Analyzing credit reports and financial statements

- Assessing property value and potential investment risk

- Ensuring compliance with federal lending regulations

- Protecting both lender and borrower financial interests

By working collaboratively, these professionals transform a complex financial evaluation into a structured, transparent process that helps homebuyers in Oakland County, Michigan, and beyond achieve their homeownership goals while maintaining responsible lending practices.

Essential Components of the Mortgage Approval Process

The mortgage approval process is a systematic evaluation involving multiple critical components that collectively determine a borrower’s financial eligibility and loan viability. Understanding these essential elements helps potential homebuyers in Oakland County, Michigan, navigate the complex landscape of home financing more effectively.

Financial Documentation Requirements

Comprehensive financial documentation forms the foundational layer of mortgage approval. Lenders require an extensive set of documents that provide a transparent view of a borrower’s financial health, income stability, and potential lending risk.

Key financial documents typically include:

- Proof of income (W2 forms, tax returns, pay stubs)

- Bank statements covering recent months

- Investment account statements

- Documentation of additional income sources

- Comprehensive employment verification

According to the Consumer Financial Protection Bureau, these documents help lenders assess a borrower’s ability to repay the proposed mortgage loan.

Credit and Risk Assessment

Beyond documentation, lenders conduct an extensive evaluation of a borrower’s credit profile and risk potential. This assessment goes beyond a simple credit score, involving a nuanced analysis of financial behaviors, existing debt obligations, and overall economic stability.

Critical risk assessment factors include:

- Credit score and credit history depth

- Debt-to-income ratio

- Payment history on existing financial obligations

- Length of credit history

- Types of existing credit accounts

By thoroughly examining these elements, lenders develop a comprehensive understanding of a borrower’s financial reliability and potential lending risk, ensuring responsible mortgage allocation in the real estate market.

Factors Influencing Mortgage Approval Decisions

Mortgage approval decisions are complex evaluations that extend far beyond simple numerical assessments. Lenders consider a sophisticated array of financial and personal factors to determine a borrower’s lending risk and potential for successful loan repayment, especially in competitive real estate markets like Oakland County, Michigan.

Financial Stability Indicators

Financial stability represents the cornerstone of mortgage approval considerations. Lenders meticulously analyze multiple indicators that demonstrate a borrower’s economic reliability and long-term financial health.

Key financial stability factors include:

- Consistent and verifiable income streams

- Employment history and job stability

- Total annual earnings

- Predictable revenue patterns

- Demonstrated ability to manage existing financial obligations

These indicators help lenders assess the likelihood of consistent mortgage payments and reduce potential default risks.

Risk Mitigation Strategies

Mortgage approval decisions incorporate sophisticated risk mitigation strategies that protect both the lender and the borrower. Credit worthiness plays a pivotal role in this assessment, with multiple interconnected elements determining overall financial reliability.

Critical risk evaluation components consist of:

- Credit score and comprehensive credit history

- Debt-to-income ratio analysis

- Payment history on existing financial commitments

- Length and diversity of credit experiences

- Current outstanding debt levels

According to Fannie Mae’s underwriting guidelines, these factors collectively provide a holistic view of a borrower’s financial management capabilities and potential lending risk, ensuring responsible and strategic mortgage allocation in the real estate marketplace.

Understanding the Timeline of the Mortgage Approval Process

The mortgage approval process is a multifaceted journey that unfolds through distinct phases, each with its own unique timeline and critical milestones. For homebuyers in Oakland County, Michigan, understanding this progression helps set realistic expectations and navigate the complex landscape of home financing more effectively.

Initial Application and Preliminary Review

The initial phase of mortgage approval begins with the submission of a comprehensive loan application. This critical stage involves providing detailed financial documentation and initiating the lender’s preliminary assessment of a borrower’s financial profile.

Key components of this initial stage include:

- Completing the official mortgage application

- Submitting required financial documentation

- Authorizing credit history review

- Providing employment and income verification

- Initial credit score assessment

Typically, this preliminary review can take 3-5 business days, during which lenders conduct an initial evaluation of the borrower’s financial standing.

Comprehensive Underwriting and Verification

Following the initial review, the application enters the detailed underwriting phase. This stage represents the most intensive period of financial scrutiny, where lenders conduct an exhaustive examination of the borrower’s financial health and the proposed property’s value.

Critical verification steps during this period include:

- Comprehensive credit report analysis

- Detailed income and employment verification

- Property appraisal and valuation

- Debt-to-income ratio calculation

- Risk assessment and final lending decision

According to Freddie Mac’s mortgage guidelines, this comprehensive underwriting process typically spans 30-45 days, depending on the complexity of the borrower’s financial profile and the specific lending institution’s procedures.

The following table outlines the primary phases of the mortgage approval process, including each stage’s typical timeline and main activities. This helps clarify what to expect during each step from application to final decision.

| Phase | Typical Timeline | Main Activities |

|---|---|---|

| Initial Application & Preliminary Review | 3–5 business days | Application submission, borrower document collection, and initial credit review. |

| Comprehensive Underwriting & Verification | 30–45 days | In-depth credit and income analysis, property appraisal, and detailed risk verification. |

| Final Approval & Closing | Varies (few days) | Final loan decision issued, preparation of closing documents, and funding of the loan. |

Ready for Mortgage Approval Clarity? Let a Local Expert Guide Your Next Move

Navigating the mortgage approval process can feel overwhelming. If you are stressing about financial documentation or worried about hidden hurdles during underwriting, you are not alone. Many buyers feel confusion or uncertainty as they try to match lender expectations with their own dreams of owning a home in Oakland County. The good news is that you do not have to interpret all these steps and requirements alone. This is where proven local expertise makes all the difference.

Work with a trusted Oakland County Realtor who breaks down the mortgage process in plain language and advocates for your unique needs. When you connect with Tom Gilliam, you get personalized support for every stage of home buying, whether you are searching for Farmington Hills homes for sale or evaluating properties in Novi, Northville, or West Bloomfield. If you want to avoid costly mistakes and reach your homeownership goals faster, visit homes2moveyou.com today. Take the first step now and turn complex mortgage steps into smooth progress toward your next home.

Frequently Asked Questions

What is the mortgage approval process?

The mortgage approval process is a financial evaluation conducted by lenders to determine if a borrower qualifies for a home loan, assessing their financial stability, credit history, and repayment capacity.

What documents do I need for mortgage approval?

You will typically need to provide proof of income, recent bank statements, tax returns, employment verification, and any documentation of additional income sources for mortgage approval.

How long does the mortgage approval process take?

The initial application and preliminary review can take 3-5 business days, while the comprehensive underwriting and verification phase usually spans 30-45 days, depending on the lender’s procedures.

What factors influence mortgage approval decisions?

Lenders consider financial stability indicators like consistent income, debt-to-income ratio, credit score, and overall financial history when making mortgage approval decisions.

Recommended

Check out this article next