Understanding Flood Insurance Michigan for Homeowners

Floods can devastate a home in minutes and most people do not realize that a single inch of floodwater can cause over $25,000 in property damage. You might think homeowners insurance has you covered for this kind of disaster. The truth is, nearly all standard policies exclude flood damage entirely. That means the difference between peace of mind and crushing financial loss can come down to a specific policy you probably have not thought about: flood insurance.

Table of Contents

- What Is Flood Insurance And How Does It Work?

- Why Flood Insurance Matters For Home Buyers And Sellers

- Key Considerations For Flood Insurance In Oakland County

- Understanding Flood Zones And Risk Assessment

- How To Evaluate Flood Insurance Options For Your Property

Quick Summary

| Takeaway | Explanation |

|---|---|

| 1. Flood insurance is essential | Standard homeowners insurance does not cover flood damage, making separate flood insurance crucial for property protection. |

| 2. Purchase separately through NFIP | In Michigan, flood insurance must be obtained outside of a typical homeowners policy, often via the National Flood Insurance Program. |

| 3. Evaluate local flood risks | Review your property’s flood zone classification and historical data to understand potential risks before purchasing insurance. |

| 4. Flood insurance impacts real estate value | Having proper coverage can enhance property value and attract buyers, making it a critical factor in real estate decisions. |

| 5. Consider comprehensive coverage options | Compare NFIP policies with private insurers to find the best flood insurance solution tailored to your property and financial needs. |

Table: Key takeaways for Michigan homeowners on why flood insurance matters and how it impacts property value and real estate investments.

What is Flood Insurance and How Does It Work?

Flood insurance provides specialized financial protection for property owners against damages caused by flooding events. Unlike standard homeowners insurance policies, flood insurance offers targeted coverage specifically for water-related property damage that occurs when water overflows from natural bodies of water, heavy rainfall, or storm surge.

Understanding Basic Flood Insurance Coverage

Flood insurance operates as a distinct financial product designed to protect homeowners from substantial financial losses. According to the National Flood Insurance Program, these policies typically cover two primary areas:

- Direct physical damage to your home’s structure

- Damage to personal property and contents inside the home

In Michigan, residents face unique flood risks due to the state’s numerous lakes, rivers, and proximity to the Great Lakes. The coverage helps homeowners recover from devastating water damage that can result in tens of thousands of dollars in repairs.

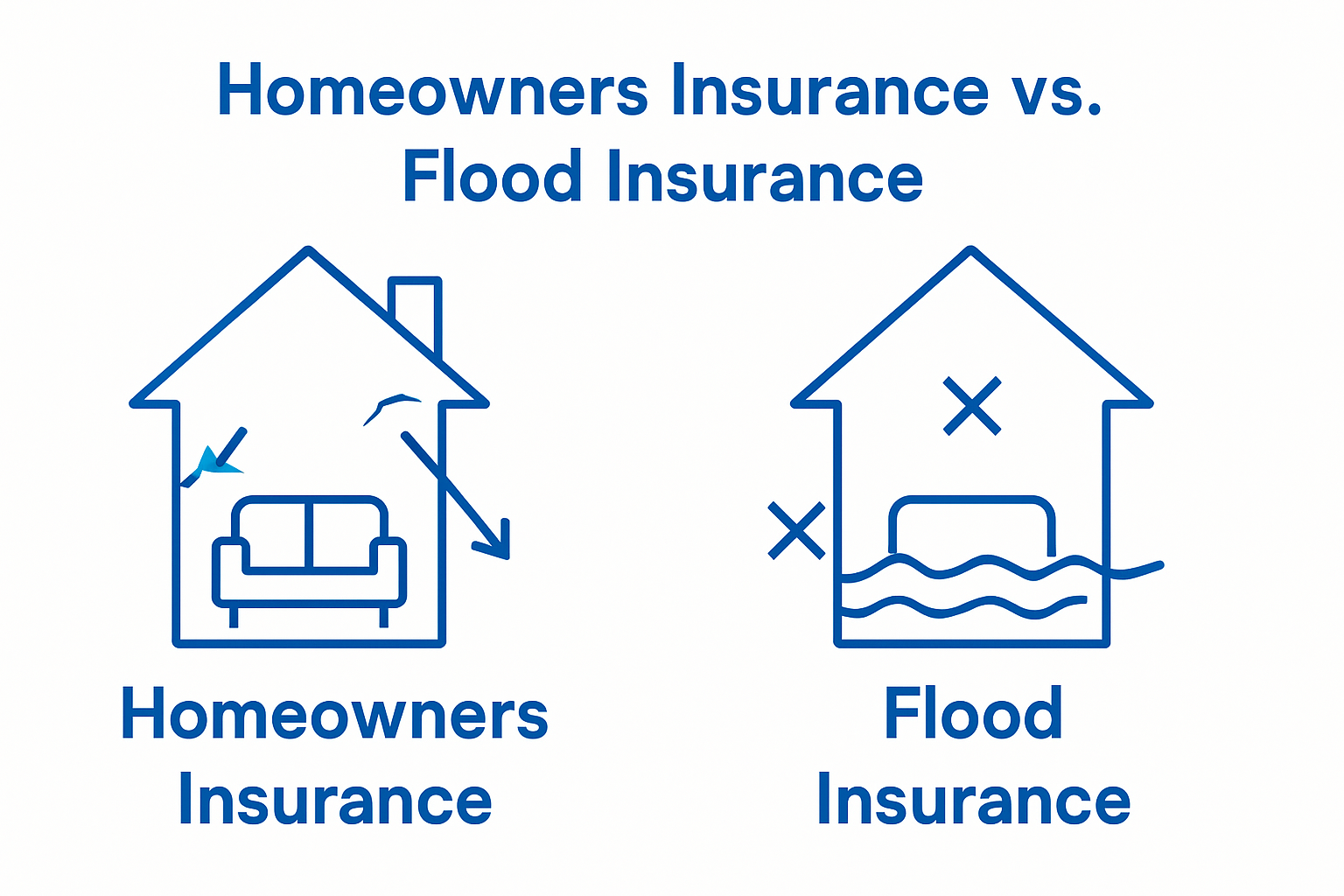

How Flood Insurance Differs from Standard Homeowners Insurance

Traditional homeowners insurance policies generally exclude flood damage, making flood insurance a critical additional protection for property owners. In Michigan, homeowners must purchase flood insurance separately through the National Flood Insurance Program or private insurers.

Key differences include:

- Standard homeowners insurance does not cover flood-related damages

- Flood insurance requires a separate policy with a typical 30-day waiting period

- Coverage limits and premiums vary based on flood zone risk assessments

Below is a comparison table highlighting the key differences between standard homeowners insurance and flood insurance as discussed in the article.

| Feature | Standard Homeowners Insurance | Flood Insurance |

|---|---|---|

| 1. Flood Damage Coverage | Not included under standard homeowners policies. | Specifically covered when purchased as a separate flood policy. |

| 2. Purchase Requirement | Included automatically in most home purchases. | Required in high-risk flood zones and must be purchased separately. |

| 3. Provider Options | Available through standard insurance providers. | Offered through the National Flood Insurance Program (NFIP) and private insurers. |

| 4. Waiting Period | No special waiting period beyond standard claim rules. | Typically requires a 30-day waiting period before coverage begins. |

| 5. Coverage Limits | Varies by policy but excludes flood-related damages. | Determined by flood zone, insurer, and property value. |

| 6. Premium Cost Influences | Based on risks like fire, theft, liability, and property age. | Impacted by local flood risk, property location, and FEMA zone classification. |

| 7. Required for Mortgages | Yes, required for most mortgage loans. | Yes, required if the property is located in a designated flood hazard area. |

Table: Comparison of standard homeowners insurance versus flood insurance, highlighting coverage differences, costs, and mortgage requirements for Michigan homeowners.

As Michigan’s Department of Environment, Great Lakes, and Energy explains, flood insurance is crucial for protecting your most significant investment against unpredictable water-related risks. Homeowners in areas like Oakland County, including cities such as Farmington Hills, Novi, and West Bloomfield, should carefully evaluate their flood risk and consider comprehensive flood insurance coverage.

Why Flood Insurance Matters for Home Buyers and Sellers

Flood insurance plays a critical role in real estate transactions, offering significant financial protection and risk mitigation for both home buyers and sellers in Michigan. Understanding its importance can help homeowners make informed decisions about property investments and protect their financial interests.

Financial Risk Management for Buyers

For home buyers, flood insurance represents a crucial element of comprehensive property protection. Mortgage lenders often require flood insurance in designated high-risk areas, making it an essential consideration during the home purchasing process. FEMA’s flood risk maps provide crucial information about potential flood zones, helping buyers assess potential risks before making a property investment.

Key considerations for home buyers include:

- Evaluating the property’s flood zone classification

- Understanding potential annual flood insurance costs

- Assessing long-term financial implications of flood risks

Impact on Property Value and Marketability

For home sellers in Oakland County, flood insurance can significantly influence a property’s market value and attractiveness to potential buyers. Properties with existing flood insurance coverage and documented low-risk status can command higher market prices and attract more interested buyers. Proactive flood insurance documentation can streamline the selling process and provide transparency about the property’s risk profile.

Important seller considerations include:

- Obtaining current flood zone certification

- Maintaining comprehensive flood insurance records

- Demonstrating property flood mitigation efforts

As Michigan State University’s Extension Office explains, flood insurance is not just a financial safeguard but a strategic asset in real estate transactions. Homeowners in flood-prone regions like Farmington Hills, Novi, and West Bloomfield must recognize that comprehensive flood coverage protects both their physical property and their financial investment.

Key Considerations for Flood Insurance in Oakland County

Oakland County homeowners face unique flood risks that require careful evaluation and strategic insurance planning. Understanding local geographical nuances and potential water-related hazards is crucial for selecting appropriate flood insurance coverage that provides comprehensive protection.

Identifying Local Flood Risk Zones

Michigan’s diverse landscape, particularly in Oakland County, presents varied flood risk profiles across different municipalities. FEMA’s flood risk maps serve as essential tools for homeowners to assess their specific property’s vulnerability. Municipalities like Farmington Hills, Novi, and West Bloomfield have distinct geographical characteristics that influence flood potential.

Key flood risk assessment factors include:

- Proximity to rivers, lakes, and drainage systems

- Historical flood data for specific neighborhoods

- Local topographical variations

- Recent infrastructure and drainage improvements

Insurance Coverage and Cost Strategies

Homeowners must carefully evaluate flood insurance options that balance comprehensive protection with affordable premiums. The National Flood Insurance Program offers standard coverage, but private insurers may provide additional flexibility for Oakland County residents.

Important coverage considerations include:

- Building property coverage limits

- Personal property protection levels

- Replacement cost versus actual cash value

- Deductible options and their financial implications

As you explore moving to Oakland County, understanding flood insurance becomes a critical component of responsible homeownership. The Michigan Department of Environment, Great Lakes, and Energy recommends that homeowners conduct thorough risk assessments and maintain updated insurance documentation to protect their significant investment.

Understanding Flood Zones and Risk Assessment

Flood zones represent critical geographical classifications that determine a property’s potential flood risk, directly impacting insurance requirements and homeowner preparedness.

In Michigan, these designations provide essential insights into the likelihood of water-related property damage and help residents make informed decisions about flood insurance coverage.

Flood Zone Classification System

FEMA’s flood zone mapping categorizes areas based on their probability of flooding, using a comprehensive system that evaluates historical water levels, topographical features, and potential environmental risks. Oakland County properties are assigned specific zone designations that reflect their unique geographical characteristics.

The following table summarizes the main flood zone categories referenced in the article and their associated risk levels for homeowners in Michigan.

| Flood Zone Category | Risk Level | Description |

|---|---|---|

| 1. High-Risk SFHA | High | Special Flood Hazard Areas (SFHA) with a significant likelihood of flooding and mandatory flood insurance requirements. |

| 2. Moderate-Risk Zones | Moderate | Areas with some potential for flooding; insurance is not federally required but strongly recommended. |

| 3. Low-Risk Zones | Low | Regions with minimal flooding risk; flood insurance is typically optional but may still offer valuable protection. |

| 4. Undetermined Risk Areas | Unknown | Zones where flood risk has not been fully assessed, leaving property owners uncertain of their exposure. |

Table: FEMA flood zone categories explained, outlining risk levels from high to undetermined for Michigan homeowners considering flood insurance.

Key flood zone categories include:

- High-risk Special Flood Hazard Areas (SFHA)

- Moderate-risk zones with potential flood conditions

- Low-risk zones with minimal flooding probability

- Undetermined risk zones requiring further assessment

Risk Assessment Strategies for Homeowners

Effective flood risk assessment goes beyond simple zone classification, requiring a holistic approach that considers multiple environmental and structural factors. Homeowners in regions like Farmington Hills, Novi, and West Bloomfield must evaluate several critical elements to understand their true flood vulnerability.

Comprehensive risk assessment involves:

- Analyzing local watershed and drainage infrastructure

- Reviewing historical flood data for specific neighborhoods

- Evaluating property elevation and surrounding terrain

- Consulting professional flood risk assessments

As Michigan State University’s Extension Office recommends, residents should leverage local resources for moving to Oakland County while simultaneously understanding their specific flood risk profile. Proactive assessment and insurance planning can significantly mitigate potential financial losses and provide peace of mind for homeowners navigating Michigan’s complex environmental landscape.

How to Evaluate Flood Insurance Options for Your Property

Evaluating flood insurance options requires a strategic approach that considers multiple factors specific to your property, location, and financial circumstances. Michigan homeowners must navigate a complex landscape of coverage choices to ensure comprehensive protection against potential water-related damages.

Comparing Insurance Coverage Types

FEMA’s flood insurance guidance outlines two primary coverage pathways for homeowners: National Flood Insurance Program (NFIP) policies and private market insurance offerings. Understanding the nuanced differences between these options is crucial for making an informed decision.

Key coverage comparison factors include:

- Standard NFIP policy limits and restrictions

- Private insurer flexibility and additional coverage options

- Pricing structures and premium calculations

- Specific exclusions and policy limitations

Financial Considerations and Risk Assessment

Homeowners in Oakland County must conduct a comprehensive financial evaluation that extends beyond basic premium costs. This involves assessing potential flood risks, property value, and the long-term financial implications of different insurance strategies.

Critical financial assessment elements include:

- Total potential replacement costs for property and contents

- Annual insurance premium affordability

- Deductible levels and their financial impact

- Potential out-of-pocket expenses during flood events

As you explore moving to Oakland County, understanding the intricate details of flood insurance becomes paramount. The Michigan Department of Insurance recommends that homeowners in flood-prone regions like Farmington Hills, Novi, and West Bloomfield conduct thorough research and consult with insurance professionals to develop a tailored flood protection strategy that meets their unique needs.

Protect Your Investment With Expert Guidance on Flood Risk and Real Estate

Are you concerned about unexpected water damage and the financial strain floods can place on your Oakland County home? The article discussed the gaps in standard homeowners policies and the unique risks Michigan homeowners face, especially in places like Farmington Hills, Novi, and West Bloomfield. Figuring out flood zones and insurance requirements can be stressful and confusing, particularly when your family’s security is on the line.

If you want peace of mind and expert support for your next home purchase or sale, partner with a local professional who understands the challenges of flood insurance in Michigan. At Homes2MoveYou, Tom Gilliam uses in-depth market knowledge and years of Oakland County experience to guide you through every detail, from moving to Oakland County to evaluating risks and protecting your investment. Secure your future, clarify your options, and let us help you confidently navigate the flood insurance process. Start your real estate journey with trusted, personalized guidance by visiting Homes2MoveYou today.

Frequently Asked Questions

What is flood insurance and how does it work?

Flood insurance provides financial protection for property owners against damages caused by flooding events, covering direct physical damage to a home’s structure and personal property.

How does flood insurance differ from standard homeowners insurance?

Flood insurance specifically covers flood-related damages, which are typically excluded from standard homeowners insurance policies, requiring a separate policy purchase.

Why is flood insurance important for home buyers in flood-prone areas?

Flood insurance is essential for home buyers as mortgage lenders often require it in designated high-risk areas, helping protect against financial loss from potential flooding.

What factors should homeowners consider when evaluating flood insurance options?

Homeowners should assess property value, potential replacement costs, insurance coverage types (NFIP vs. private insurers), annual premiums, and deductible levels to make informed decisions.

Recommended

Check out this article next