Understanding Closing Costs: What You Need to Know

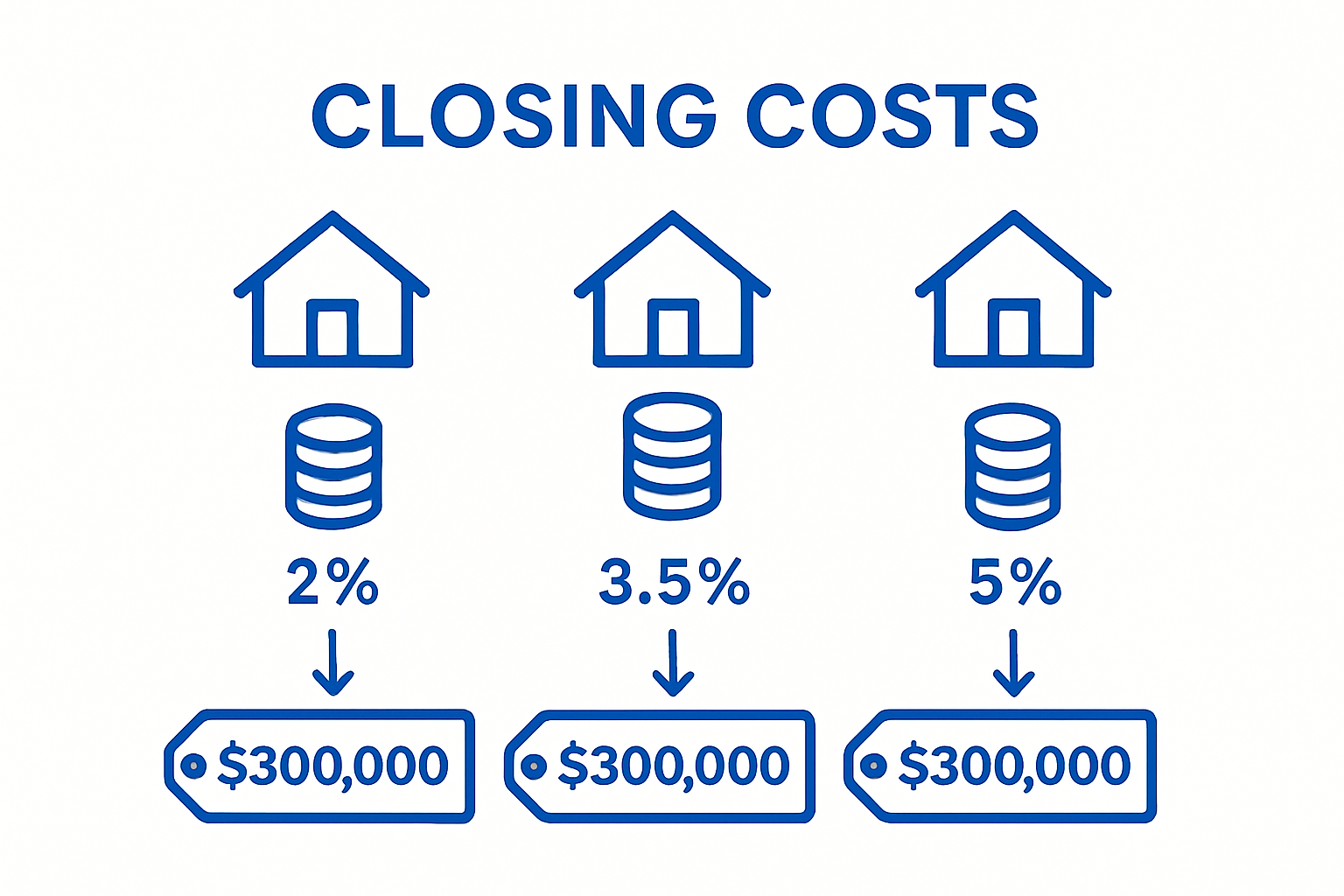

Most home buyers focus on the price tag when searching for a new place in Oakland County. But here is the shocker. Closing costs can tack on an extra 2% to 5% of a home’s price, meaning $6,000 to $15,000 on a $300,000 house. Many buyers are caught off guard by these numbers and miss out on smart ways to manage them.

Table of Contents

- What Are Closing Costs And Why They Matter

- Key Components Of Closing Costs Explained

- How Closing Costs Affect Home Buyers And Sellers

- Understanding The Role Of Closing Agents And Fees

- Tips For Managing And Reducing Closing Costs

Quick Summary

For many Oakland County homebuyers, closing costs can be an unexpected surprise if not planned for in advance. These fees—ranging from 2% to 5% of the purchase price—cover everything from lender charges to legal and title expenses. Understanding how closing costs work, how to negotiate them, and how to compare options helps buyers budget effectively and avoid last-minute stress. The table below outlines the most important takeaways every buyer should know.

| Takeaway | Explanation |

|---|---|

| Know Your Closing Costs | Closing costs typically range from 2% to 5% of the purchase price, making them a key part of financial planning. |

| Break Down Costs by Category | Common expenses include lender fees, appraisals, title and legal services, government charges, and property surveys. |

| Negotiate Seller Contributions | Buyers can request sellers to cover part of the closing costs, reducing upfront expenses and easing budget strain. |

| Compare Lender Fees | Request estimates from multiple lenders to identify competitive rates and minimize unnecessary charges. |

| Select an Experienced Closing Agent | A knowledgeable closing agent helps streamline the process, minimizing risks of delays and costly errors. |

What Are Closing Costs and Why They Matter

Closing costs represent the additional expenses beyond the property’s purchase price that buyers and sellers must pay to complete a real estate transaction. These financial obligations are crucial to understand because they can significantly impact your overall home buying budget and final transaction expenses.

Understanding the Financial Landscape

Closing costs typically range between 2% to 5% of a home’s total purchase price. For Oakland County real estate, this means on a $300,000 home, you might expect to pay between $6,000 and $15,000 in closing expenses. These costs cover various administrative, legal, and processing fees required to transfer property ownership.

Key Components of Closing Costs

Closing costs encompass multiple elements that facilitate the real estate transaction:

- Lender Fees: Mortgage origination charges, credit report fees, and application processing expenses

- Property Evaluation Fees: Appraisal and home inspection costs

- Title and Legal Expenses: Title search, insurance, and attorney fees

- Government Recording Fees: Local and state document registration charges

Understanding these components helps homebuyers prepare financially for the complete investment required in purchasing a property. While closing costs might seem overwhelming, they represent essential steps in securing a smooth property transfer and protecting all parties involved in the transaction.

In the Oakland County real estate market, working with an experienced local realtor can help you navigate and potentially negotiate some of these expenses. Buyers should always budget for these additional costs to avoid financial surprises during the final stages of home purchasing.

Key Components of Closing Costs Explained

Closing costs represent a complex financial landscape that encompasses numerous fees and expenses beyond the property’s purchase price. Understanding these components is crucial for buyers and sellers to accurately budget and prepare for their real estate transaction.

Breaking Down Lender and Financial Fees

Lender fees constitute a significant portion of closing costs and include several critical financial charges. Mortgage origination fees typically range from 0.5% to 1% of the total loan amount, covering the lender’s administrative expenses for processing your mortgage application. Credit report fees, which usually cost between $30 and $50, allow lenders to review your creditworthiness and financial history.

Property Evaluation and Legal Expenses

Property-related expenses form another essential category of closing costs. Home appraisal fees in Oakland County generally run between $300 and $500, providing an independent assessment of the property’s market value.

Title search and insurance costs, which protect against potential ownership disputes, can range from $500 to $1,500. Mortgage advice experts recommend setting aside funds specifically for these evaluation and legal expenses.

Additional critical closing cost components include:

- Government Recording Fees: Charges for officially documenting property transfer

- Survey Fees: Expenses for verifying property boundaries and land measurements

- Escrow Fees: Charges for third-party management of financial transactions

- Transfer Taxes: Local and state taxes associated with property ownership transfer

In the Oakland County real estate market, these fees can vary based on local regulations and specific transaction details. Homebuyers should work closely with their realtor to anticipate and budget for these expenses, ensuring a smooth and financially prepared property acquisition process.

To help readers quickly understand the essential elements that make up closing costs, the table below summarizes each key component along with its typical cost range in the Oakland County market.

Closing costs can feel overwhelming for many Oakland County homebuyers, but breaking them down by category makes them easier to understand and plan for. From lender fees and appraisals to title services and transfer taxes, each component plays a role in the total amount due at closing. The table below outlines the most common closing cost components, their purpose, and typical cost ranges to help you budget confidently for your next home purchase.

| Component | Description | Typical Cost/Range |

|---|---|---|

| Lender Fees | Origination charges, credit report fees, and application processing costs. | 0.5%–1% of loan; $30–$50 |

| Property Evaluation Fees | Includes professional appraisals and home inspections required by lenders. | $300–$500 |

| Title & Legal Expenses | Title search, title insurance, and attorney fees to verify ownership and protect against disputes. | $500–$1,500 |

| Government Recording Fees | Official charges for recording and registering the property transaction. | Typically $50–$200 |

| Survey Fees | Costs for verifying property boundaries and confirming accurate land measurements. | $300–$700 |

| Escrow Fees | Third-party management fees for handling financial transactions securely. | $400–$700 |

| Transfer Taxes | Local and state taxes charged when property ownership is transferred. | 0.5%–2% of purchase price |

How Closing Costs Affect Home Buyers and Sellers

Closing costs represent a critical financial consideration that significantly impacts both home buyers and sellers during real estate transactions. Understanding these expenses helps parties make informed decisions and strategically navigate the complex financial landscape of property transfers.

Financial Impact on Home Buyers

For home buyers, closing costs can represent a substantial upfront expense beyond the property’s purchase price. Typically ranging from 2% to 5% of the total home value, these costs can add thousands of dollars to the initial investment. In Oakland County, this means a $300,000 home could incur closing costs between $6,000 and $15,000, potentially challenging buyers’ financial preparation.

Negotiation Strategies and Cost Allocation

Buyers and sellers have multiple strategies to manage closing costs. Some approaches include:

- Seller Concessions: Sellers might agree to cover a portion of the buyer’s closing expenses

- Rolled Closing Costs: Some lenders allow buyers to incorporate closing costs into their mortgage

- Lender Credits: Borrowers can sometimes negotiate lower upfront costs in exchange for a slightly higher interest rate

Michigan home prices comparison demonstrates how regional market dynamics can influence closing cost negotiations. In competitive markets like Oakland County, buyers might have less leverage, while in slower markets, sellers could be more willing to contribute to closing expenses.

Sellers also experience financial implications from closing costs. They typically pay real estate agent commissions, which can range from 5% to 6% of the home’s sale price, significantly impacting their net proceeds. Understanding these financial nuances helps both parties plan more effectively and approach real estate transactions with greater confidence.

To clarify available options for managing closing costs, the table below compares popular strategies buyers and sellers can use, along with the main benefits and considerations for each.

In Oakland County’s competitive housing market, both buyers and sellers can use smart strategies to manage or reduce closing costs. From negotiating seller concessions to leveraging lender credits, these options provide flexibility in how fees are handled at the closing table. The table below highlights the most common strategies, who typically uses them, their benefits, and key considerations to keep in mind.

| Strategy | Who Uses It | Benefit | Consideration |

|---|---|---|---|

| Seller Concessions | Buyer / Seller | Helps buyers reduce upfront cash needed at closing. | Requires seller agreement; may affect offer competitiveness. |

| Rolled Closing Costs | Buyer | Allows buyers to roll closing fees into the loan, lowering immediate out-of-pocket expenses. | Increases total loan balance and long-term monthly payments. |

| Lender Credits | Buyer | Reduces or eliminates upfront closing costs by trading for a slightly higher interest rate. | Raises long-term borrowing costs over the life of the loan. |

| Agent Commission Split | Seller / Agent | May reduce seller’s total closing costs tied to agent commissions. | Could impact agent motivation or reduce seller’s net proceeds. |

Understanding the Role of Closing Agents and Fees

Closing agents play a pivotal role in real estate transactions, serving as critical intermediaries who ensure the smooth transfer of property ownership. These professionals manage the complex financial and legal processes that transform a property sale from negotiation to completed transaction.

The Multifaceted Responsibilities of Closing Agents

Closing agents, often attorneys or specialized real estate professionals, coordinate numerous critical tasks during property transfers. Their primary responsibilities include verifying legal documentation, managing fund transfers, conducting title searches, and ensuring all contractual obligations are met. In Oakland County, these professionals typically charge between $500 and $1,200 for their comprehensive services, depending on the transaction’s complexity.

Financial Management and Documentation

The closing agent’s financial oversight involves several crucial steps:

- Document Verification: Reviewing and authenticating all legal paperwork

- Fund Disbursement: Managing the transfer of funds between buyer, seller, and relevant financial institutions

- Title Insurance Coordination: Ensuring proper title transfer and protecting against potential ownership disputes

- Tax and Fee Calculation: Precisely calculating and distributing required government and transaction fees

Mortgage rate effects can significantly influence the closing process, making the closing agent’s role even more critical in navigating complex financial landscapes. These professionals act as neutral third parties, guaranteeing that all transaction requirements are met accurately and efficiently.

In the Oakland County real estate market, selecting an experienced closing agent can mean the difference between a smooth property transfer and a potentially complicated transaction. Their expertise helps protect both buyers and sellers by ensuring all legal and financial aspects of the property sale are handled with professional precision.

Tips for Managing and Reducing Closing Costs

Managing closing costs requires strategic planning and proactive financial preparation. Homebuyers in Oakland County can employ several effective techniques to minimize these expenses and optimize their real estate investment strategy.

Strategic Negotiation and Comparison

Comparing lender fees is a critical first step in reducing closing costs. Homebuyers should request detailed loan estimates from multiple financial institutions, analyzing not just interest rates but also associated closing expenses. In the Oakland County market, this approach can potentially save hundreds to thousands of dollars by identifying more competitive fee structures.

Cost-Saving Strategies and Techniques

Homebuyers can implement multiple approaches to manage closing expenses:

- Shop Around for Services: Compare prices for title insurance, home inspections, and other required services

- Negotiate Seller Contributions: Request sellers to cover portions of closing costs

- Leverage Lender Credits: Consider slightly higher interest rates in exchange for reduced upfront expenses

- Time Your Closing Strategically: Closing at month’s end can minimize prepaid interest charges

Michigan property investment strategies often emphasize the importance of minimizing transaction costs. Experienced buyers understand that reducing closing expenses directly impacts overall investment returns.

Understanding the nuanced landscape of closing costs empowers buyers to make informed financial decisions. By approaching the process strategically, homebuyers can significantly reduce their upfront expenses while maintaining the integrity of their real estate transaction in the competitive Oakland County market.

Take the Confusion Out of Closing Costs With Local Expertise

Worried about unexpected closing costs and how they can impact your home buying or selling experience in Oakland County? Understanding lender fees, appraisal charges, title expenses, and more is essential if you want to manage your budget and prevent last-minute surprises. If navigating these complex costs feels overwhelming, you are not alone. Many buyers and sellers in Farmington Hills and nearby communities have the same concerns.

Partner with a trusted local expert who can guide you through every step. Tom Gilliam has over 20 years of experience helping clients understand and minimize their closing costs while achieving their real estate goals. Secure your financial peace-of-mind by choosing a knowledgeable Farmington Hills Realtor who truly puts your best interests first. Ready to move forward with confidence? Visit https://homes2moveyou.com today and schedule your personalized consultation before you commit to your next transaction.

Frequently Asked Questions

What are closing costs in real estate transactions?

Closing costs are the additional expenses beyond the property’s purchase price that buyers and sellers must pay to complete a real estate transaction. They typically range from 2% to 5% of the home’s total purchase price and cover various administrative, legal, and processing fees.

What are the main components of closing costs?

The main components of closing costs include lender fees (such as mortgage origination charges), property evaluation fees (appraisal and inspection costs), title and legal expenses (title search and insurance), government recording fees, survey fees, escrow fees, and transfer taxes.

How can buyers manage and reduce closing costs?

Buyers can manage and reduce closing costs by shopping around for competitive lender fees, negotiating seller contributions, leveraging lender credits, and strategically timing the closing date to minimize prepaid interest charges.

How do closing costs affect home buyers and sellers financially?

Closing costs represent a substantial upfront expense for home buyers, often adding thousands of dollars to their initial investment. For sellers, these costs can include agent commissions, impacting their net proceeds from the sale. Understanding these expenses helps both parties make informed decisions during the transaction.

Recommended

Check out this article next