FHA Loans Explained: Key Benefits, Rules, and Process

Did you know that FHA loans allow buyers to purchase a home with as little as 3.5 percent down? This flexible option opens doors for many people in Oakland County who might struggle to qualify for conventional mortgages. With only modest credit and steady income, first-time buyers often find FHA loans create a smoother path to homeownership. Understanding how these government-backed mortgages work empowers you to make the best decision for your financial future.

Key Takeaways

| Point | Details |

|---|---|

| Accessible Financing | FHA loans allow for lower credit scores and down payments, making homeownership attainable for low to moderate-income borrowers. |

| Mortgage Insurance Requirement | Borrowers must pay both upfront and monthly mortgage insurance premiums, which can affect long-term costs. |

| Property Standards | Homes must meet strict condition requirements, limiting options for buyers and necessitating thorough inspections. |

| Comparison with Other Loans | FHA loans are often more favorable for first-time buyers compared to conventional, VA, and USDA loans in terms of eligibility and down payment. |

Table of Contents

- Defining FHA Loans And Core Concepts

- Eligibility Requirements And Documentation Needed

- Key Benefits And Limitations For Buyers

- Typical FHA Loan Costs And Fees

- FHA Vs. Conventional And Other Loan Types

- Step-By-Step FHA Loan Process In Oakland County

Defining FHA Loans And Core Concepts

Federal Housing Administration (FHA) loans represent a powerful mortgage option designed to make homeownership more accessible, especially for first-time buyers and those with modest financial backgrounds. Government-backed mortgages provide unique advantages that set them apart from traditional lending approaches.

According to Investopedia, these specialized loans enable borrowers to finance up to 96.5% of a home’s value with flexible credit requirements. The key qualification metrics include:

- Minimum credit score of 580 allows for a 3.5% down payment

- Credit scores between 500-579 require a 10% down payment

- Must use the property as a primary residence

- Can finance up to four-unit properties if occupying one unit

As FHA.com explains, these loans are government-guaranteed through the Department of Housing and Urban Development (HUD). This guarantee provides critical protections for lenders, enabling them to offer more lenient qualification standards compared to conventional mortgages. For Oakland County homebuyers struggling with traditional lending requirements, FHA loans represent a strategic pathway to homeownership.

Eligibility Requirements And Documentation Needed

FHA loan eligibility involves several key financial and personal requirements that set these government-backed mortgages apart from conventional lending options. Oakland County homebuyers should understand that these loans are specifically designed to support low to moderate-income borrowers who might face challenges with traditional mortgage standards.

According to Investopedia, the primary credit score requirements are straightforward:

- Minimum 580 credit score qualifies for 3.5% down payment

- Credit scores between 500-579 require a 10% down payment

- Scores below 500 typically do not qualify

Refi.com highlights that FHA loans offer more flexibility with debt-to-income ratios and employment history. This means borrowers with non-traditional career paths or higher debt loads can still secure financing. Typical documentation you’ll need includes:

- Proof of steady employment (2 years of tax returns)

- Current pay stubs

- Bank statements

- Social Security number

- Valid government-issued identification

Prospective borrowers must also demonstrate the property will serve as their primary residence, which means living in the home for at least one year after purchase. For Oakland County residents exploring homeownership, FHA loans offer a strategic pathway with more inclusive qualification standards.

Key Benefits And Limitations For Buyers

FHA loans offer a unique blend of advantages and potential drawbacks that Oakland County homebuyers should carefully consider. Mortgage accessibility takes center stage with these government-backed loan options, providing opportunities for individuals who might struggle with traditional lending standards.

According to Zillow, the key benefits include:

- Down payments as low as 3.5%

- More lenient credit score requirements

- Flexible debt-to-income ratio standards

- Loan assumability for future home sellers

- Eligibility for streamline refinancing

Chase highlights some critical limitations buyers must understand. Mortgage insurance is a significant consideration, with borrowers required to pay both upfront and monthly premiums. These insurance costs can potentially last the entire loan duration, depending on the initial down payment amount.

Additionally, FHA loans come with stricter property condition requirements. Homes must pass comprehensive inspections and meet specific standards, which can limit buyer options in Oakland County’s diverse real estate market. While these requirements protect buyers from purchasing properties with significant defects, they can also complicate the home buying process. For first-time homebuyers or those with limited financial resources, these loans represent a strategic pathway to homeownership, balancing accessibility with protective measures.

Typical FHA Loan Costs And Fees

Understanding the complete financial landscape of FHA loan expenses is crucial for Oakland County homebuyers planning their mortgage strategy. These government-backed loans come with specific fee structures that differ significantly from conventional mortgage options.

According to Capital One, FHA loans involve two primary mortgage insurance premium components:

- Upfront Mortgage Insurance Premium (UFMIP): 1.75% of total loan amount

- Annual Mortgage Insurance Premium (MIP): Ranges from 0.45% to 1.05% of loan balance

LendingTree emphasizes that borrowers cannot avoid these insurance premiums, regardless of their down payment size. The upfront premium can typically be rolled into the loan amount, providing some initial financial flexibility. For Oakland County buyers, this means carefully calculating the total loan cost beyond the base mortgage price.

Buyers should also budget for additional standard closing costs, which might include appraisal fees, title insurance, and origination charges.

While FHA loans offer more accessible financing, the ongoing mortgage insurance premiums represent a long-term financial commitment. Interestingly, borrowers making a down payment of 10% or more might see their annual mortgage insurance premium cancelable after 11 years, offering a potential future cost-saving opportunity for strategic homebuyers.

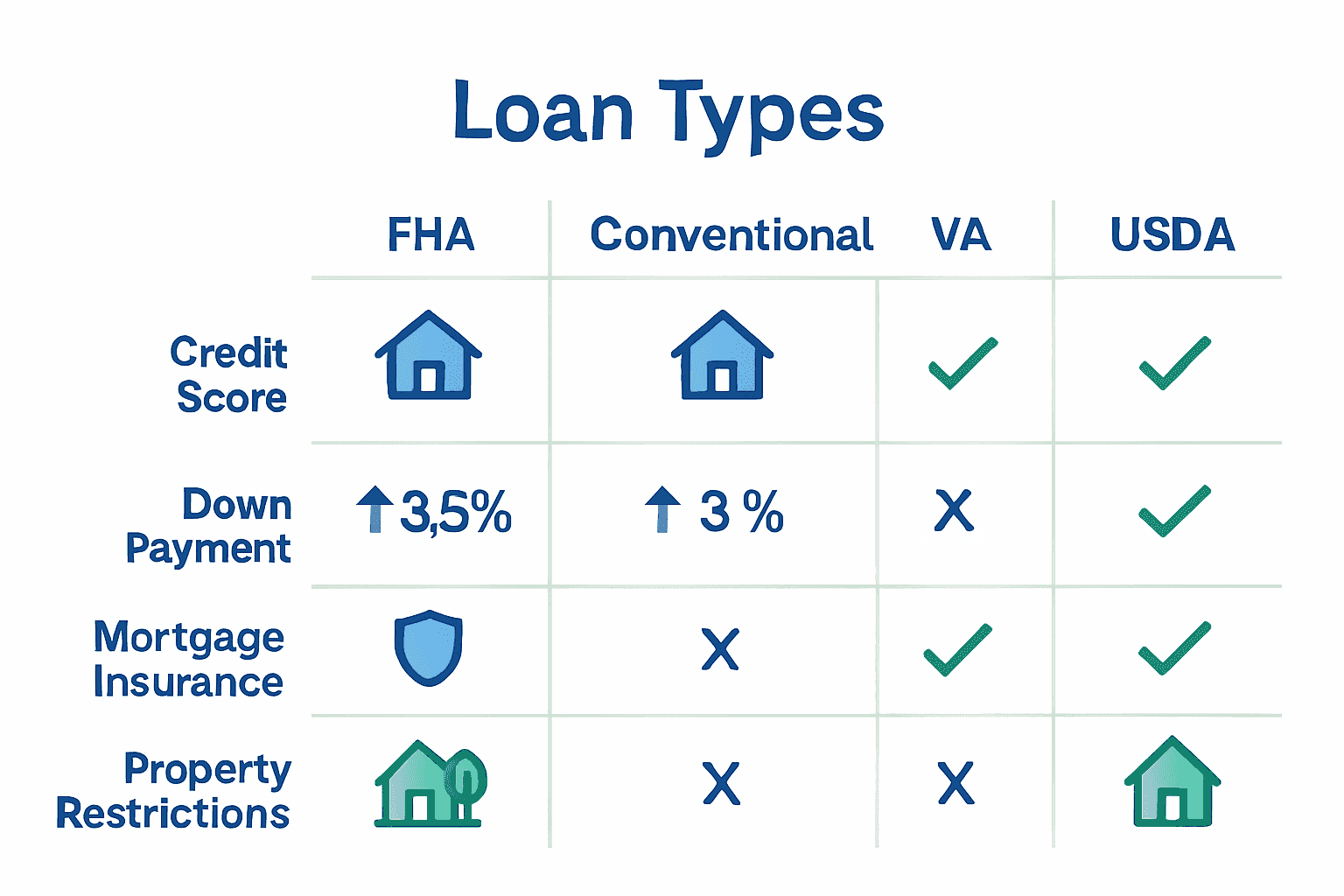

FHA Vs. Conventional And Other Loan Types

Navigating the mortgage landscape requires understanding the nuanced differences between loan types, particularly for Oakland County homebuyers seeking the most advantageous financing strategy. Each mortgage option presents unique benefits tailored to different financial situations and homeownership goals.

According to Chase, key distinctions between FHA and conventional loans include:

- FHA Loans:

- More lenient credit requirements

- Lower down payment options

- Mandatory mortgage insurance

- Stricter property standards

- Conventional Loans:

- Higher credit score requirements

- Mortgage insurance removable with 20% equity

- Higher loan limits

- More flexible property conditions

Investopedia highlights additional specialized loan options for Oakland County residents:

- VA Loans: For veterans, offering no private mortgage insurance

- USDA Loans: Zero down payment for rural property purchases

- Jumbo Loans: Designed for high-value property financing

For first-time homebuyers or those with modest financial backgrounds, FHA loans often provide the most accessible path to homeownership. While they come with specific constraints, these government-backed mortgages offer a strategic entry point into the real estate market, especially for individuals who might not qualify for conventional financing.

Here’s how FHA loans compare to Conventional, VA, and USDA loans:

| Loan Feature | FHA Loans | Conventional Loans | VA Loans | USDA Loans |

|---|---|---|---|---|

| Credit Score Requirement | 500–580+ | 620+ | Typically 620+ | 640+ |

| Down Payment | 3.5% (minimum) | 3%–20% | 0% (no down payment required) | 0% (no down payment required) |

| Mortgage Insurance | Required (upfront + monthly) | Required if <20% down | None required | None required |

| Eligible Borrowers | First-time or low/moderate-income buyers | Strong credit and stable income borrowers | Veterans, active-duty, and eligible spouses | Low-to-moderate-income buyers in rural areas |

| Property Requirements | Must meet FHA appraisal standards | Standard appraisal and condition requirements | Property must be safe and habitable | Must be in USDA-eligible rural/suburban area |

| Loan Limits (2025 – Oakland County) | Up to $498,257 (approx.) | Varies by lender and credit | Typically matches conforming loan limits | Dependent on income and property location |

| Best For | Buyers with limited savings or lower credit | Borrowers with strong credit and higher down payments | Eligible veterans seeking zero-down financing | Buyers in eligible rural/suburban communities |

5%-10% | 3%-20% | 0% | 0% |

5%-10% | 3%-20% | 0% | 0% |

| Mortgage Insurance | Required (upfront & annual) | Required if <20% down, removable | None | Required |

| Property Restrictions | Primary residence, condition limits | More flexible | Eligible veterans only | Rural properties only |

| Loan Assumability | Yes | Rare | Yes | Yes |

Step-By-Step FHA Loan Process In Oakland County

Navigating the FHA loan application in Oakland County requires strategic preparation and understanding of the local real estate landscape. Prospective homebuyers should approach this process methodically, ensuring they have all necessary documentation and financial insights ready.

Initial Preparation Steps

- Check and improve credit score

- Gather financial documentation

- Calculate your debt-to-income ratio

- Determine your home buying budget

Detailed Application Process

The journey begins with a comprehensive financial review. Borrowers must collect critical documents including:

- Two years of tax returns

- Recent pay stubs

- Bank statements

- Proof of employment

- Social Security documentation

Once documentation is assembled, applicants should explore mortgage loan options specific to Oakland County. Working with a local FHA-approved lender who understands the nuanced Michigan real estate market can significantly streamline the process.

The final stages involve a comprehensive home appraisal and property inspection, specific to FHA standards. Homes must meet strict condition requirements, which can be particularly important in Oakland County’s diverse housing market. Borrowers should budget for potential repair negotiations or property modifications to satisfy FHA inspection protocols. Patience and thorough preparation are key to successfully navigating this government-backed mortgage pathway.

Ready to Unlock FHA Loan Benefits with a Local Expert?

Navigating FHA loans can be overwhelming, especially if you are concerned about qualifying, understanding strict property standards, or preparing the right documents. The road to affordable homeownership is full of complex choices and rules, as discussed in our guide to FHA Loans Explained. If you have ever felt frustrated by strict lender requirements or worried about mortgage insurance premiums, you are not alone. These hurdles can seem intimidating if you are a first-time buyer or have unique financial needs in Oakland County.

Imagine having a seasoned Realtor by your side, guiding you through every requirement and helping you seize all the benefits FHA loans offer. With over 20 years of success in Farmington Hills and the surrounding areas, Tom Gilliam makes it easy to move forward. Whether you are searching for expert help with Oakland County mortgage loan options or want tailored support as a buyer or seller, you can count on clear answers and proven results. Visit homes2moveyou.com now to connect with Tom and take your next confident step toward homeownership. Opportunities in this market will not wait, so act now and get ahead of the competition.

Frequently Asked Questions

What are FHA loans?

FHA loans are government-backed mortgages designed to make homeownership more accessible, especially for first-time buyers and those with modest financial backgrounds. They offer flexible credit requirements and low down payment options.

What are the eligibility requirements for FHA loans?

To qualify for an FHA loan, borrowers typically need a minimum credit score of 580 to make a 3.5% down payment. Those with scores between 500-579 must make a 10% down payment, and the property must be used as a primary residence.

What are the key benefits of FHA loans?

FHA loans offer several advantages, including lower down payments (as low as 3.5%), more lenient credit score requirements, flexible debt-to-income ratio standards, and the ability to assume the loan in the future.

What costs should I expect when applying for an FHA loan?

FHA loans involve costs such as an Upfront Mortgage Insurance Premium (UFMIP) of 1.75% and an Annual Mortgage Insurance Premium (MIP) that ranges from 0.45% to 1.05% of the loan balance. Additionally, there are standard closing costs to consider, such as appraisal fees and title insurance.

Recommended