Understanding What is Mortgage Insurance and Its Importance

Buying a home with less than a 20 percent down payment might seem out of reach for many people in Oakland County. Yet more than 50 percent of first-time buyers put down less than 20 percent and still get approved for mortgages. Sounds risky for banks, right? That risk is actually managed by mortgage insurance, and the biggest surprise is that this extra protection opens the door for thousands of families to own homes much sooner than they ever thought possible.

Table of Contents

- Defining Mortgage Insurance: What It Is

- Why Mortgage Insurance Matters for Homeowners

- How Mortgage Insurance Works: The Basics Explained

- Types of Mortgage Insurance and Their Implications

- Real-World Context: Mortgage Insurance in Oakland County

Quick Summary

Understanding mortgage insurance is essential for today’s homebuyers in Oakland County and across Michigan. While often viewed as just another expense, mortgage insurance opens the door to homeownership with lower down payments, protects lenders, and helps buyers build equity over time. The table below highlights the key takeaways and explanations every buyer should know about how mortgage insurance works and why it matters in competitive real estate markets.

| Takeaway | Explanation |

|---|---|

| Mortgage insurance enables lower down payments. | Homebuyers can qualify for a mortgage with less than 20% down, increasing access to homeownership opportunities. |

| Types of mortgage insurance vary by loan type. | Conventional loans often require Private Mortgage Insurance (PMI), while FHA and VA loans follow different structures. |

| Premium costs are influenced by multiple factors. | Credit score, down payment percentage, and loan type all impact monthly mortgage insurance costs. |

| Mortgage insurance supports long-term financial stability. | While an added expense, it allows homeowners to build equity and pursue long-term financial planning goals. |

| Local real estate conditions affect mortgage insurance choices. | Competitive housing markets make it essential to understand lender requirements and optimize insurance strategies. |

Defining Mortgage Insurance: What It Is

Mortgage insurance represents a financial protection mechanism designed to safeguard lenders when homebuyers cannot provide a standard 20% down payment. Understanding this unique insurance product helps homeowners navigate complex lending requirements and access homeownership opportunities.

The Basic Concept of Mortgage Insurance

At its core, mortgage insurance is a risk mitigation tool for lenders. When homebuyers contribute less than 20% of a property’s purchase price as a down payment, they are typically required to obtain mortgage insurance. This insurance protects the lender in case the borrower defaults on their mortgage loan.

According to Consumer Financial Protection Bureau, mortgage insurance lowers the risk to the lender, enabling borrowers to qualify for loans they might not otherwise obtain. The key aspects of mortgage insurance include:

- Protects the lender’s financial investment

- Enables lower down payment options

- Typically required for conventional loans with less than 20% down

How Mortgage Insurance Works

Mortgage insurance operates differently depending on the loan type. For conventional loans, private mortgage insurance (PMI) is standard. Government-backed loans like FHA and VA loans have their own mortgage insurance structures. The insurance premium is usually added to the monthly mortgage payment and can be removed once the homeowner builds sufficient equity.

The cost of mortgage insurance varies based on several factors:

- Down payment percentage

- Credit score

- Loan type

- Property value

- Loan term

While mortgage insurance represents an additional expense for homebuyers, it serves a critical function in expanding homeownership opportunities by allowing individuals to purchase homes with smaller down payments. Understanding its mechanics helps potential homeowners make informed financial decisions about their mortgage strategy.

Why Mortgage Insurance Matters for Homeowners

Mortgage insurance plays a critical role in expanding homeownership opportunities for individuals who might otherwise struggle to enter the real estate market. By providing financial protections and risk mitigation strategies, this insurance mechanism transforms homeownership possibilities for many buyers across Oakland County and beyond.

Bridging the Down Payment Gap

One of the most significant benefits of mortgage insurance is its ability to help homebuyers overcome the traditional 20% down payment barrier. In expensive real estate markets like Farmington Hills and Novi, saving substantial upfront funds can seem impossible for many working professionals and first-time homeowners.

According to Freddie Mac, mortgage insurance enables buyers to purchase homes with substantially lower initial investments. Key advantages include:

- Reducing initial cash requirements

- Accelerating homeownership timelines

- Providing flexibility for emerging homebuyers

Financial Protection and Risk Management

Mortgage insurance serves dual purposes for both lenders and homeowners. For lenders, it mitigates potential financial losses if a borrower defaults. For homeowners, it represents an opportunity to build equity and establish long-term financial stability.

The insurance premium calculations consider multiple risk factors:

- Credit score

- Down payment percentage

- Income stability

- Property location

- Loan term length

While mortgage insurance represents an additional monthly expense, it ultimately creates pathways to homeownership that would otherwise remain closed. By understanding its mechanics, potential homebuyers can make informed decisions about their real estate investments and financial futures.

How Mortgage Insurance Works: The Basics Explained

Mortgage insurance is a sophisticated financial mechanism that enables homebuyers to secure loans with minimal down payments while protecting lenders from potential financial risks. Understanding its intricate operational framework helps potential homeowners make informed decisions about their real estate investments.

Types of Mortgage Insurance

Mortgage insurance varies significantly depending on the loan type and lending institution. Two primary categories dominate the market: private mortgage insurance (PMI) for conventional loans and government-backed mortgage insurance for federal loan programs. Each type comes with unique requirements, premium structures, and coverage specifications.

According to Fannie Mae, mortgage insurance programs serve critical functions in expanding homeownership opportunities by mitigating lender risks. The primary mortgage insurance variations include:

- Borrower-paid mortgage insurance

- Lender-paid mortgage insurance

- Single premium mortgage insurance

- Split premium mortgage insurance

Premium Calculation and Payment Structures

Mortgage insurance premiums are calculated using complex algorithms that assess multiple risk factors. Lenders evaluate an individual’s creditworthiness, down payment amount, loan type, and overall financial profile to determine insurance costs. These premiums can be structured as monthly payments, upfront lump sums, or hybrid arrangements.

Key factors influencing mortgage insurance premiums include:

- Credit score range

- Down payment percentage

- Loan-to-value ratio

- Property type

- Loan term duration

While mortgage insurance represents an additional expense, it provides a critical pathway for homebuyers who might otherwise be unable to secure financing. By understanding the nuanced mechanics of these insurance products, potential homeowners can strategically navigate lending requirements and achieve their real estate ownership goals.

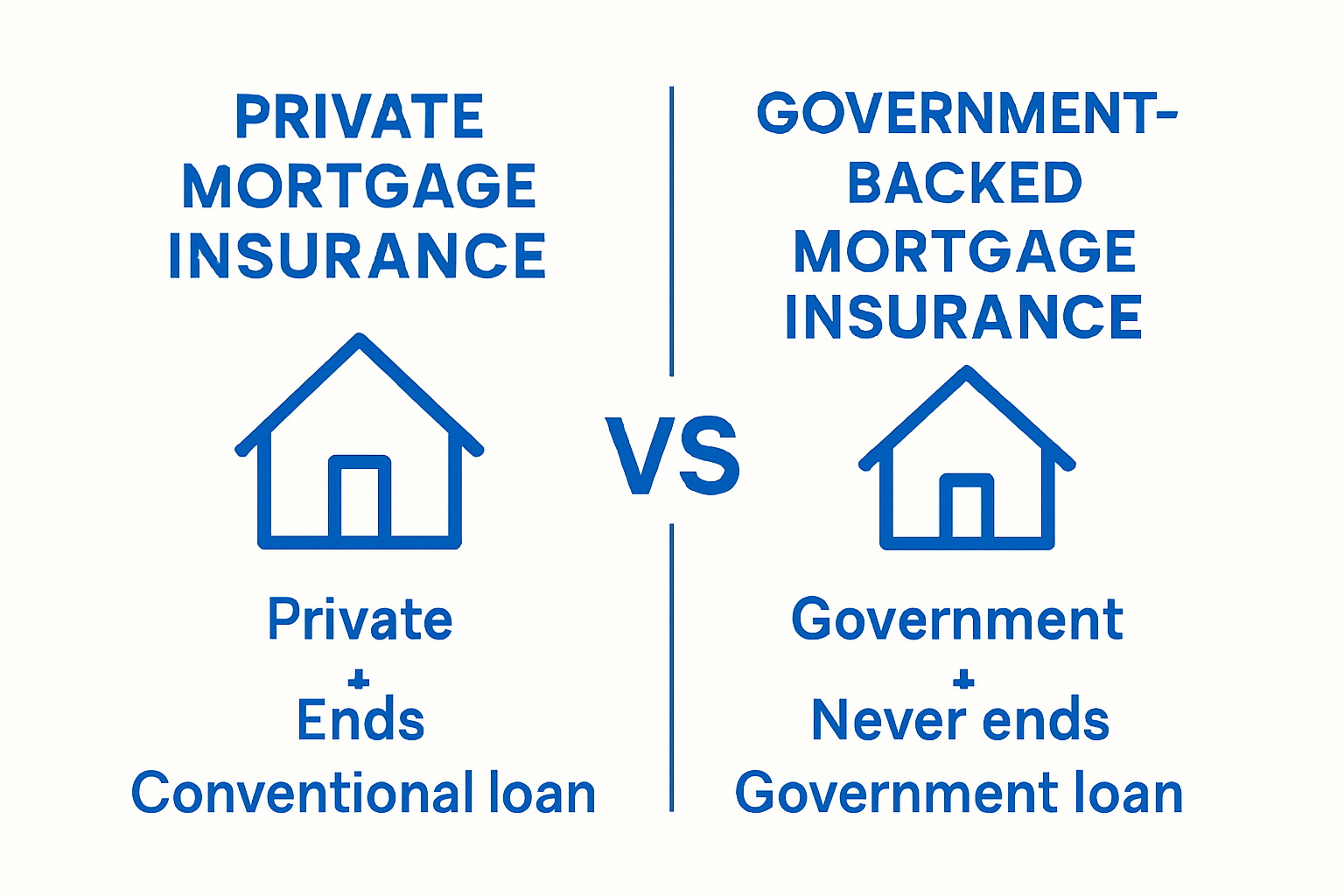

Types of Mortgage Insurance and Their Implications

Mortgage insurance represents a diverse landscape of financial protection mechanisms, each designed to address specific lending scenarios and borrower needs. Understanding the nuanced differences between various mortgage insurance types helps homebuyers make informed decisions about their real estate investments.

Private Mortgage Insurance

Private mortgage insurance (PMI) is the most common form of mortgage insurance for conventional loans. When homebuyers provide less than 20% down payment, lenders typically require PMI to mitigate potential financial risks. This insurance protects the lender if the borrower defaults, enabling more individuals to access homeownership opportunities.

According to the Consumer Financial Protection Bureau, PMI comes in several distinct formats:

- Borrower-paid mortgage insurance

- Lender-paid mortgage insurance

- Single premium mortgage insurance

- Split premium mortgage insurance

Government-Backed Mortgage Insurance

Federal loan programs offer unique mortgage insurance structures tailored to specific homebuyer demographics. FHA loans require mortgage insurance premiums (MIP) for the entire loan duration, while VA loans provide specialized coverage for military service members and veterans. USDA rural development loans also include their own mortgage insurance requirements.

Key differences in government-backed mortgage insurance include:

- Duration of insurance requirement

- Premium calculation methods

- Eligibility restrictions

- Cancellation policies

- Coverage percentage

These variations reflect the unique risk profiles and policy objectives of different federal lending programs. By understanding the specific implications of each mortgage insurance type, homebuyers can strategically navigate their financing options and select the most appropriate protection mechanism for their individual circumstances.

To help clarify the key distinctions, the following table compares private mortgage insurance (PMI) for conventional loans with government-backed mortgage insurance for federal loan programs:

For Oakland County homebuyers, understanding the different types of mortgage insurance is crucial when exploring financing options. Each loan program—whether conventional, FHA, VA, or USDA—comes with its own insurance requirements, premium structures, and rules for cancellation. Knowing these differences helps buyers choose the loan that best fits their budget and long-term goals while avoiding surprises at closing. The table below highlights the key features of each type of mortgage insurance.

| Type of Mortgage Insurance | Common Loan Types | Who Is Protected | Premium Payment Structure | Duration of Required Coverage | Unique Features |

|---|---|---|---|---|---|

| Private Mortgage Insurance (PMI) | Conventional Loans | Lender | Monthly, single, or split premium options | Cancelable once borrower reaches 20% home equity | Flexible premium formats; borrower responsible |

| FHA Mortgage Insurance | FHA Loans | Lender | Upfront Mortgage Insurance Premium (UFMIP) + monthly | Typically for life of loan, unless refinanced | Requires UFMIP at closing; higher accessibility for low-down-payment buyers |

| VA Loan Guarantee | VA Loans | Lender | One-time upfront funding fee | No monthly MI; varies by service status and loan use | Exclusive to eligible veterans, active duty, and surviving spouses |

| USDA Mortgage Insurance | USDA Rural Development Loans | Lender | Upfront guarantee fee + annual fee paid monthly | Applies for the full loan term | Designed for rural and farming-area homebuyers with income limits |

Real-World Context: Mortgage Insurance in Oakland County

Oakland County represents a unique real estate landscape where mortgage insurance plays a pivotal role in helping residents achieve homeownership. The diverse economic dynamics of communities like Farmington Hills, Novi, and West Bloomfield create nuanced mortgage insurance scenarios that require specialized understanding.

Local Market Considerations

In Oakland County, mortgage insurance becomes particularly critical due to the region’s competitive real estate market. Home prices in areas like Bloomfield Hills and Birmingham often necessitate creative financing strategies. First-time homebuyers and professionals seeking to enter these prestigious communities frequently rely on mortgage insurance to bridge financial gaps.

According to Michigan State University’s MI Money Health program, local homebuyers must carefully evaluate mortgage insurance options specific to their unique financial circumstances. Key local considerations include:

- Variability in home values across Oakland County municipalities

- Impact of local economic conditions on lending practices

- Regional differences in down payment requirements

- Specialized loan programs for metro Detroit residents

Navigating Mortgage Insurance Strategies

Homebuyers in Oakland County can leverage multiple mortgage insurance approaches to optimize their real estate investments. Understanding local lending environments helps residents make informed decisions about their mortgage insurance selections. Learn more about local mortgage financing options that can complement mortgage insurance strategies.

Regional factors influencing mortgage insurance include:

- Credit score variations

- Employment stability in metro Detroit

- Local housing market fluctuations

- Proximity to major employment centers

- Individual financial portfolio complexity

By understanding the intricate relationship between mortgage insurance and local real estate dynamics, Oakland County residents can develop sophisticated approaches to homeownership that balance financial prudence with long-term investment potential.

Ready to Make Homeownership in Oakland County a Reality?

Struggling to navigate mortgage insurance options or feeling anxious about the 20 percent down payment hurdle? You are not alone. The article addressed common pain points like uncertainty over different mortgage insurance types, how to lower upfront costs, and concerns about qualifying for a home in areas like Farmington Hills or Novi. These challenges can feel overwhelming without the right guidance.

At homes2moveyou.com, Tom Gilliam stands ready to help you decode mortgage insurance, understand your options, and secure the best possible deal for your situation. With years of real estate experience and deep local market knowledge, Tom empowers buyers to move forward with confidence. If you want to learn more about how local mortgage programs can work with your goals, visit homes2moveyou.com now. Take charge of your future and make the next step toward homeownership in Oakland County today.

Frequently Asked Questions

What is mortgage insurance?

Mortgage insurance is a financial protection mechanism that safeguards lenders when homebuyers make a down payment of less than 20% of a property’s purchase price. It mitigates the lender’s risk in case the borrower defaults on their mortgage loan.

Why do I need mortgage insurance?

Mortgage insurance is typically required by lenders for borrowers who cannot provide a standard 20% down payment. It enables individuals to access homeownership opportunities by allowing them to qualify for loans they might not otherwise obtain.

How does mortgage insurance work?

Mortgage insurance works by assigning a premium to borrowers who make a smaller down payment. The premium is usually included in the monthly mortgage payment and protects lenders against financial losses if the borrower defaults. The cost varies depending on factors like down payment percentage, credit score, and loan type.

What are the types of mortgage insurance?

There are two main types of mortgage insurance: private mortgage insurance (PMI) for conventional loans and government-backed mortgage insurance for federal loan programs like FHA and VA loans. Each type has unique requirements and premium structures.

Recommended

Check out this article next